Written by Naureen Zahid, OpenOcean's Investor Relations Director.

Note: This update was originally distributed to our Limited Partners on 22 December 2023, and all information contained herein was accurate as of this date. It is now being released to the wider audience.

Introduction

As 2023 draws to an end, we would like to continue the recent tradition we started in 2022 and provide our close network with our Macro and Market overview in which we delve into the global economic landscape, examining the pivotal moments of 2022 and the developments of 2023. We hope this will help make sense of the volatile year which we have experienced.

In this update we will provide you with our assessment and view on the current macro and market environment, highlighting key changes, and how this has been impacting public and private investments. Whilst we have tried to include the main key macroeconomic movements of the year and their impact on both public and private markets, to maintain this as non-exhaustive we have not been able to divulge everything. We would like to remind you that although this update explicitly is not investment advice and just our own review, we hope this might provide you with some information which could help assist you in forming your own views on how best to preserve and grow your capital.

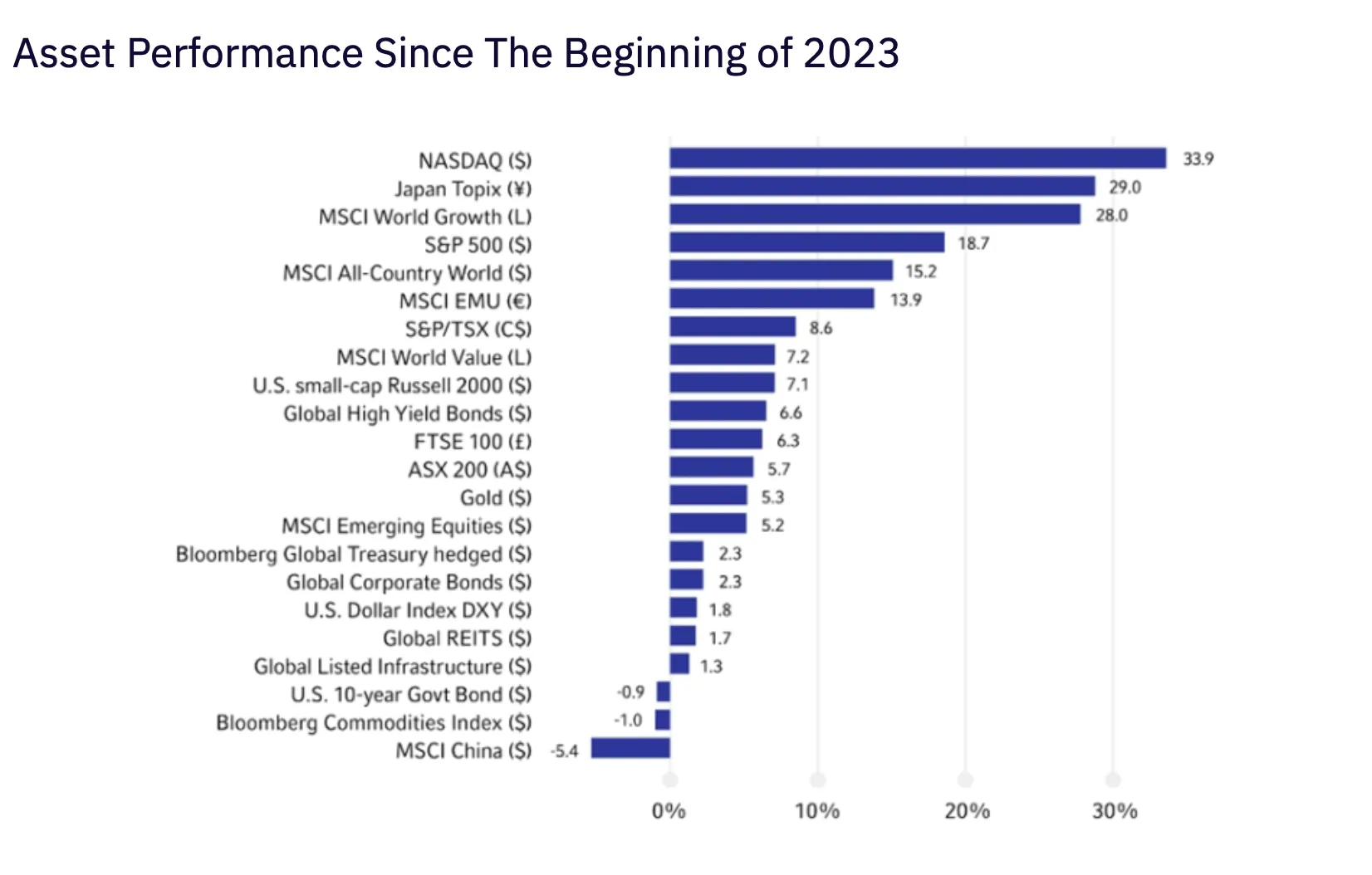

In December 2023 the S&P 500 and NASDAQ 100 are poised to set on a strong year, with their year to date returns as 24.7% and 54.77% as at 20 December 2023, and the "Magnificent Seven" (Apple, Alphabet, Facebook, Amazon, Microsoft, Tesla, Nvidia) have been the most sought-after market leaders to include in investment portfolios. Despite the positive sentiment and the rally in the equity market, it is essential not to overlook the increasing pressure on the credit sector, highlighted by the swift collapse of Silicon Valley Bank (SVB), First Republic, and Signature earlier this year, and strong concerns surrounding the US corporate and real estate debt markets.

While the upswing in equities suggests a risk-off sentiment, does this signal the conclusion of the prolonged hangover from 2020-2022? Are central banks contemplating rate cuts, and are they indicating a potential return to the Zero Interest Rate Policy (ZIRP) era?

In his seminal works "Fooled by Randomness" and "The Black Swan," former trader and risk analyst, Nassim Taleb, argues that deterministic models are inherently flawed, as they fail to account for the unpredictable nature of the world. The COVID-19 pandemic, the Russia-Ukraine war, and the recent war in the Middle East, serve as stark reminders of the limitations of deterministic thinking. These unpredictable events have had profound consequences on the global economy, challenging traditional forecasting methods and highlighting the need for a more nuanced approach to economic understanding. Through his work, Taleb advocates for a more probabilistic approach to economic decision-making, acknowledging the role of randomness and preparing for "black swan" events.

By adopting this more nuanced perspective, economic decision-makers, investors and financial systems can become more resilient to unpredictable events and mitigate risks. This is particularly important for navigating from the volatile waters of 2023, and into the complex and uncertain global economic landscape of 2024.

Macro and Market Overview

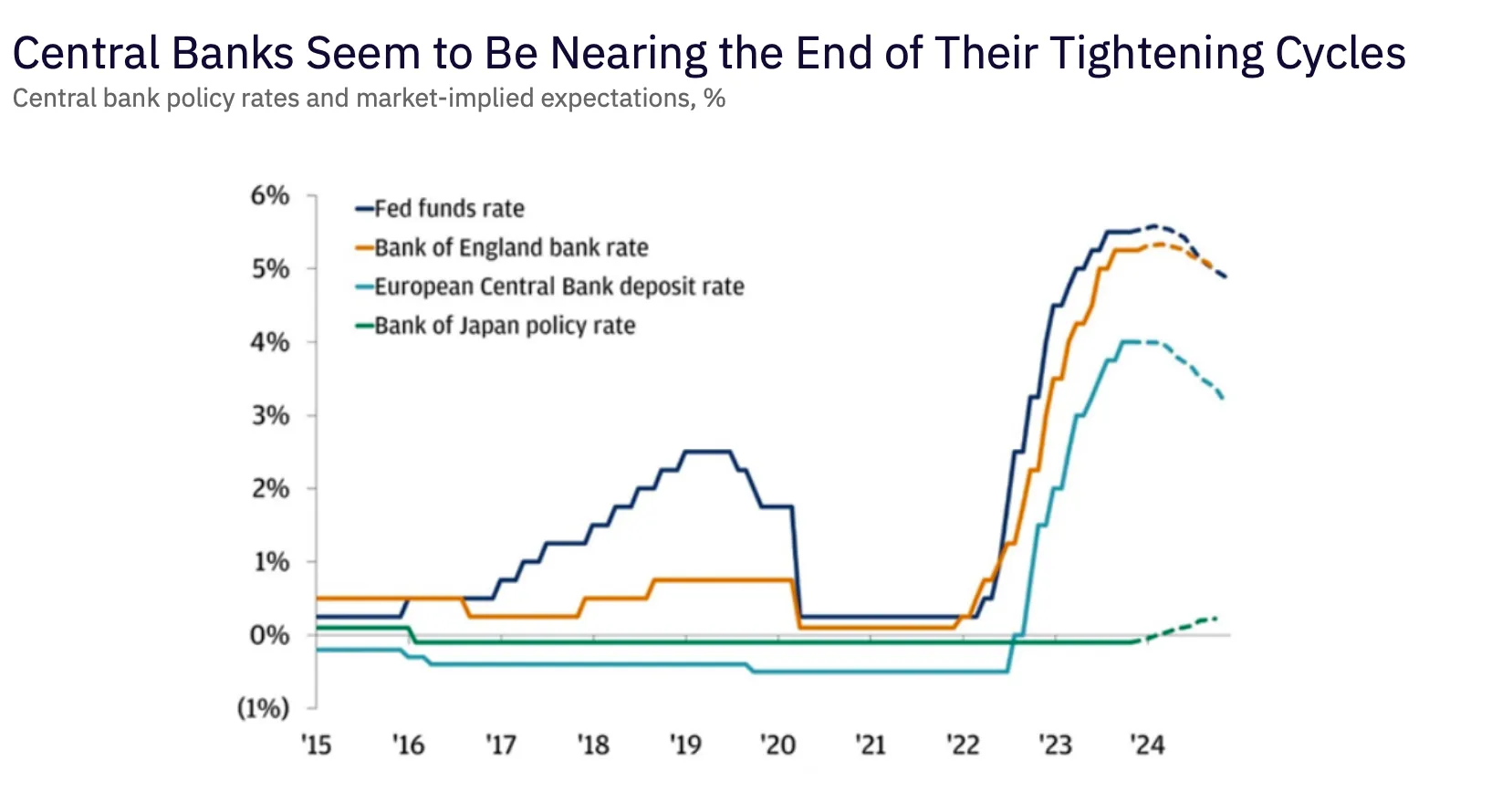

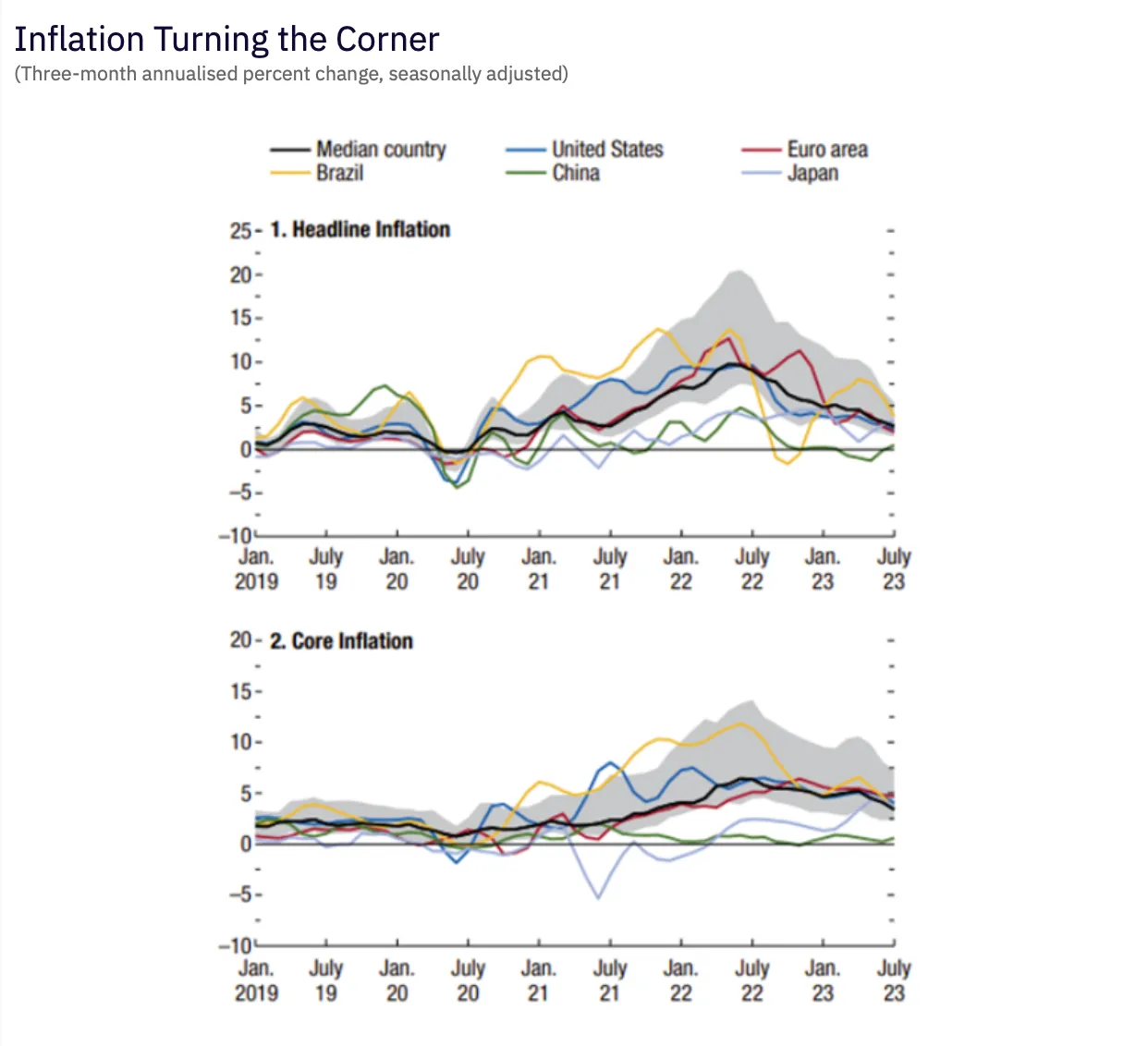

In 2023, initial predictions of an imminent Eurozone and US recession were based on indicators like an inverted US yield curve. Historical data suggested a 100% recession occurrence with inflation over 5% and unemployment under 5% painted a concerning picture. Precedents warned of challenges with an aggressive monetary policy tightening stance, as seen with the Fed in early 2022, hinting at an unavoidable hard landing for the US economy, affecting global economies.

Responding to mounting inflation concerns, major economies implemented fiscal tightening. The US Federal Reserve raised interest rates and initiated quantitative tightening (QT), reducing its balance sheet. Similarly, the European Central Bank and the Bank of England signalled tighter monetary policies, planning to raise interest rates and reduce asset purchase programs (APP). All trying to achieve their 2% inflation target rates and reducing balance sheets, including the Fed's plan to cut $47.5 billion per month, increasing to $95 billion by December 2023. The European Central Bank aimed to decrease net asset purchases to €40 billion monthly by July 2023, ending them in September 2023, whilst the Bank of England plans to reduce its asset purchase program by £10 billion monthly, concluding it in December 2023.

Fiscal tightening has a substantial impact, with higher interest rates increasing borrowing costs, potentially slowing economic growth and investment. Reductions in central bank balance sheets tighten credit conditions, making funding less accessible. Coupled with higher interest rates, this can elevate volatility in the stock market and other assets, complicating investment decisions. While fiscal tightening aims to cool an overheated economy, it introduces challenges for businesses and consumers looking to invest, necessitating careful consideration of risks and rewards.

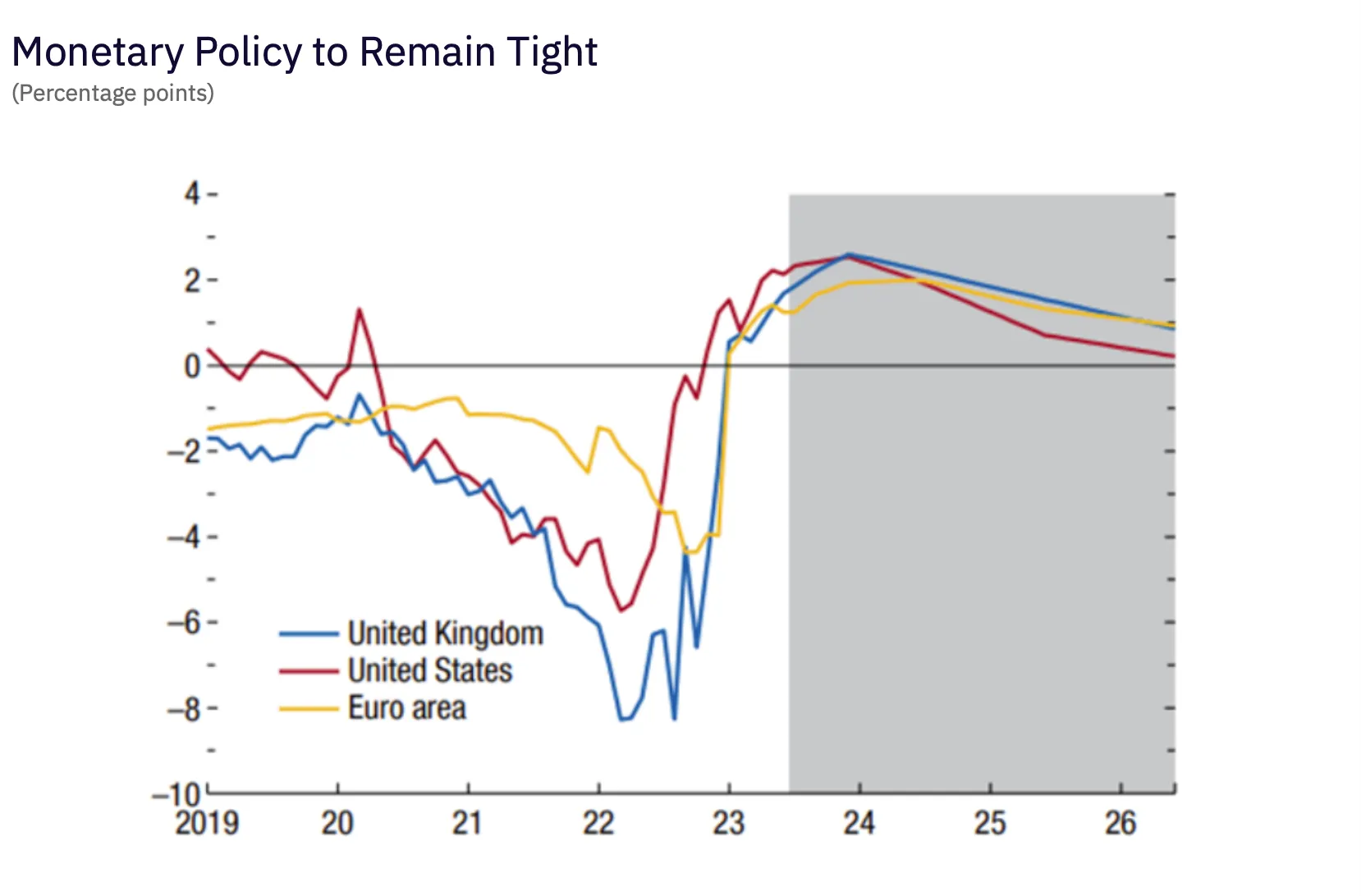

The Fed held its FOMC meeting on Wednesday 13th December and took an extremely dovish tone keeping interest rates at their current levels, and communicated its plan to hold 3 interest rate cuts during 2024, with the FOMC's "dot plot" of individual members' expectations showing expectations of the Fed funds rate to be between 2% and 2.25% by the end of 2026. This signals that the target of a “soft-landing” is achievable, whilst trying to curb inflation. However, there are many economists and investors looking back to the 1980’s, when the Fed eased monetary policy too quickly following the “Volcker Shock”, which ultimately led to a resurgence of inflation, as looser monetary conditions fuelled demand for goods and services with the decrease in borrowing costs making borrowing more attractive.

Monetary and Fiscal Policy and the “Lag Effect”

Whilst central banks have tightened monetary conditions to increase interest rates to the highest level of the last 40 years, and at the quickest pace, the effect of these higher rates do not work into the economy immediately, but are felt over a longer timeframe, and the full effect per hike can be felt typically between 6-24 months.

This is often referred to as the "lag effect", which denotes the delay between economic events or policy changes and their full reflection in market prices. Contributing factors include the time required for investors to process and interpret information, market inefficiencies, and herd behaviour. This “lag effect” poses challenges, such as potential mispricing and difficulty in timing market entry and exit points.

The impact of rising interest rates enacted in 2022 is likely to continue affecting the USA, Europe, China, and Japan in the months ahead as debts begin to roll over at higher rates leading to increased debt servicing costs and a squeeze on margins, especially with respect to corporates and consumers. Specific examples include a slowdown in the housing market due to more expensive mortgages, evidenced by falling home prices in some areas of the US. Additionally, rising interest rates initially made stocks less attractive, leading to a decline in stock prices across major markets. The bond market experienced upward pressure on yields, diminishing the value of existing bonds, notably in the US and Europe, where bond yields rose sharply in 2023; all of which impacted global investor portfolios.

The Global Picture and Impact on Growth

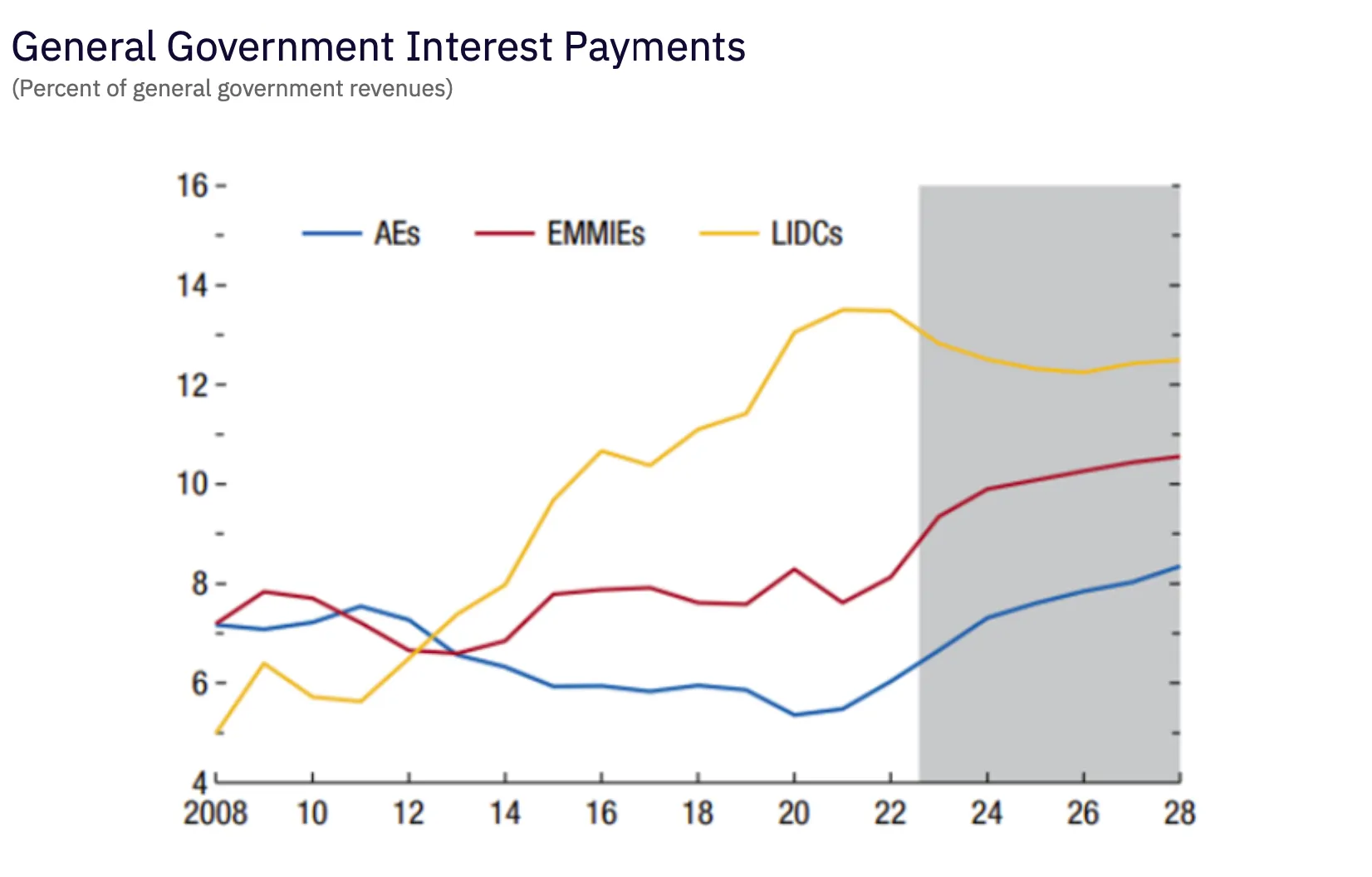

According to The World Economic Outlook, the International Monetary Fund (IMF), the global economic landscape in 2023 is characterised by a 3.4% estimated global output of approximately $3.6 trillion, presenting diverse challenges and opportunities. Developed economies like those in Europe and the UK contend with the effects of aggressive monetary tightening, creating hurdles for sustained growth. In contrast, Japan maintains an accommodative monetary policy with above-trend GDP growth. China faces mounting debt and property market concerns, showing reluctance towards aggressive stimulus measures. This complex interplay among global economic players demands careful consideration from investors and policymakers.

Distinct economic trajectories emerge across major economies. The United States experiences a resilient resurgence, anticipating GDP in 2023 surpassing pre-pandemic levels. Conversely, the Euro area struggles with a recovery, facing challenges from the Russia-Ukraine war, the recent war in the Middle East, and energy price volatility. China estimates significant output losses of around 4.2%, navigating post-pandemic slowdown and a property sector crisis, as projected by The China Banking and Insurance Regulatory Commission (CBIRC). The Office for Budget Responsibility (OBR) UK projected a five-quarter recession starting Q3 2022, with a pessimistic -1.3% annual GDP growth in 2023. These trajectories highlight the intricate challenges shaping the recovery narrative globally.

Global economic challenges persist with higher interest rates and depreciated currencies affecting low-income countries, with over half at high risk or already in distress. Europe teeters on recession, the UK faces economic challenges, while Japan stands out with accommodative policies and above-trend GDP growth. China adopts a cautious approach amid escalating debt and property market issues. These multifaceted challenges highlight the complexity of the current global economy, emphasising the need for careful thought in navigating and executing strategic decision-making.

LIDCs = low-income developing countries.

Globally, households are grappling with a real-term decline in income due to inflation, compounded by rising energy costs and elevated mortgage payments. The erosion of household and disposable income has driven many consumers to increasingly rely on debt, all of which contributes to a downward economic spiral of reduced spending, rising concerns of credit defaults and mortgage delinquencies.

This contraction in consumer spending has direct and profound implications, posing a significant threat to the global economic outlook. Anticipated declines in exports coupled with a more pronounced downturn in imports further underscore the interconnected nature of the global economy. Governments worldwide are closely monitoring this situation and its potential impact on trade, including the risk of widening trade deficits and government deficits.

This further underscores the critical importance of thoughtful economic management and the intricate relationship between fiscal policy decisions and economic variables. With J. Powell signalling three rate cuts in 2024, there is hope this negative outlook can be avoided before something breaks within the system

What This Means to Institutional Investors

Money Market Funds

In 2023, investors rapidly allocated capital to money market funds, driven by rising interest rates, geopolitical uncertainty, and a need for liquidity. Federal Reserve rate hikes enhanced the appeal of money market funds as a cash storage option, offering slightly higher interest rates than savings accounts and alternative bonds. As of October 2023, the total assets of money market funds in the United States were $4.5 trillion.

Geopolitical tensions, particularly the Russia-Ukraine war, and the recent war in the Middle East, have intensified the quest for safe-haven assets, with money market funds, backed by the U.S. government's credit, emerging as a preferred choice. Investors, attracted by high liquidity, poured a record $1.5 trillion into money market funds in H1 2023, pushing the industry's total assets to over $4.7 trillion, the highest since the early 2000s.

The flow of capital into money market funds in H1 2023 reflected a shift in investor behaviour towards safer and more liquid assets amid rising interest rates, geopolitical tensions, and a general risk-off environment.

The inflows to money market funds have slowed in H2 2023 compared to H1 2023, with total assets of money market funds in the United States being $4.5 trillion as of October 2023, representing a decrease of approximately $200 billion from the peak of $4.7 trillion in H1 2023.

Several factors have contributed to this slowdown, including the Fed slowing its pace of rate hikes in H2 2023, ultimately reducing the incentive for investors to store their money in money market funds, as they can now earn higher returns in other investments, such as bonds, or even riskier assets which offer a higher risk premia.

The three rate cuts planned by the Fed in 2024 have prompted equity markets to soar, and may stimulate investors to redeem their allocations to money market funds and seek higher returns in the equity markets.

Repo and Reverse-Repo Markets

In 2023, the increased inflows in money market funds drove the purchase of short-dated government bonds, commercial paper, and "repo" and "reverse-repo" agreements.

The repo and reverse repo markets play pivotal roles in the US financial system, facilitating short-term funding among banks and financial institutions, with significant fluctuations throughout the year closely mirroring economic changes and Federal Reserve policies.

In the repo market, institutions sell securities to counterparts, agreeing to repurchase them at a predetermined future date, resulting in temporary cash inflows against collateralised securities. This activity surged in 2023, notably in the first half, influenced by the Federal Reserve's interest rate hikes, making repo transactions attractive to banks seeking higher yields. Simultaneously, the reduction of the Federal Reserve's balance sheet led to diminished reserve liquidity, driving increased demand for repo transactions during market volatility.

The reverse repo market, involving the Fed providing cash in exchange for collateralised securities, also saw heightened activity, aligning with the strategy to drain excess liquidity and tighten monetary policy.

These market fluctuations extend beyond their immediate impact, affecting broader financial markets and investment portfolios. The increased repo market activity in the first half of 2023 contributed to an upward trend in short-term interest rates, and any disruption to repo market activity could lead to widespread liquidity issues.

The repo market serves as a barometer of investor risk appetite, with a decline indicating increased risk aversion, and is an important part of the financial system to watch in order to gauge investor sentiment. Consequently, repo and reverse repo market activity influences the returns of specific investment portfolios, especially those invested in money market funds or Treasury bills, which saw substantial inflows in 2023. As the Federal Reserve slowly loosens its monetary policy, it is anticipated that repo and reverse repo market activity may decrease, contingent on evolving economic conditions and the Fed's policy decisions.

Equity and Debt Markets, and 60/40 Portfolios

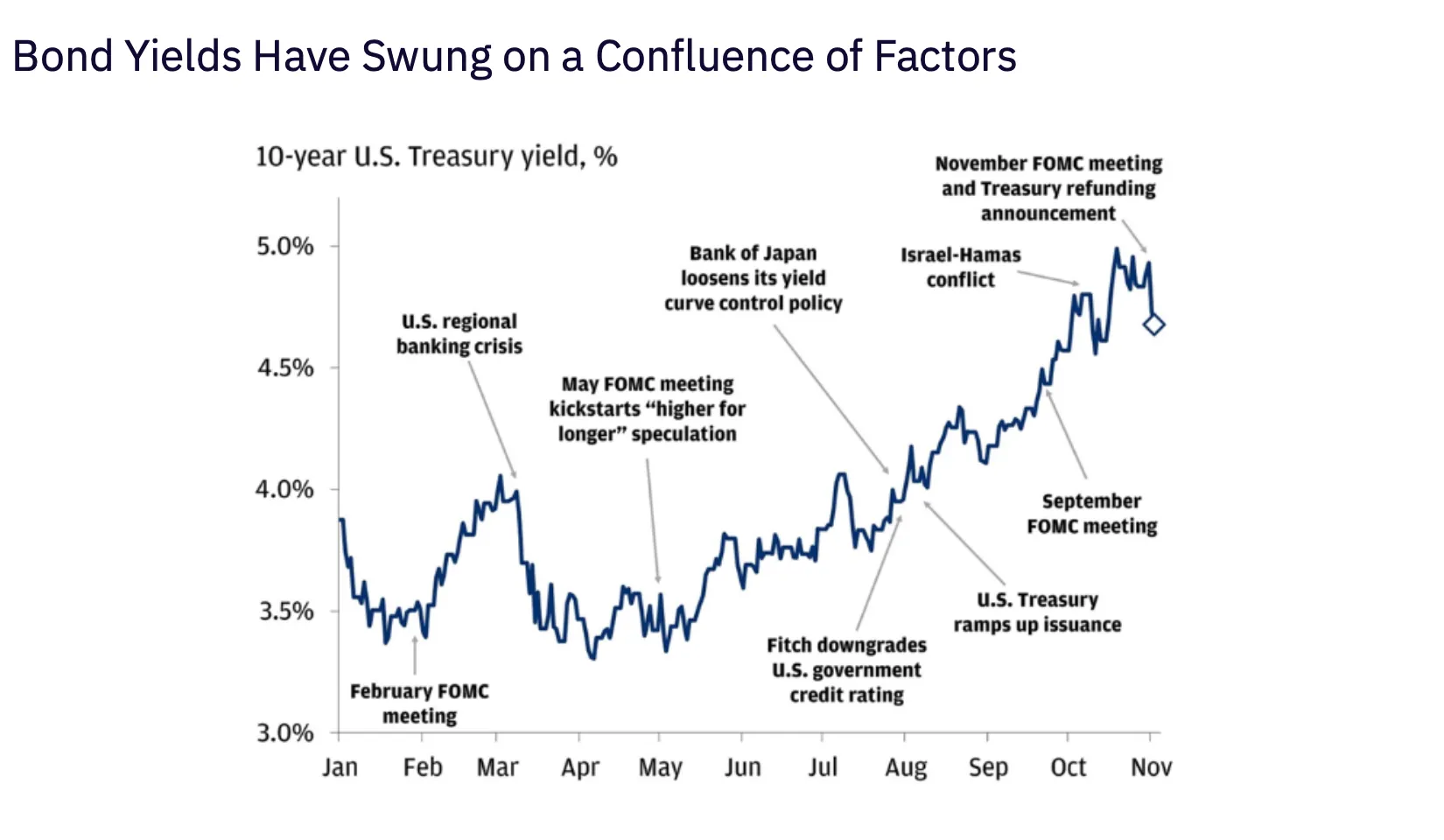

The US bond market witnessed significant volatility, reflecting the Federal Reserve's assertive measures to tighten monetary policy and combat rising inflation. Short-term, mid-term, and long-term Treasury yields all experienced substantial increases throughout the year.

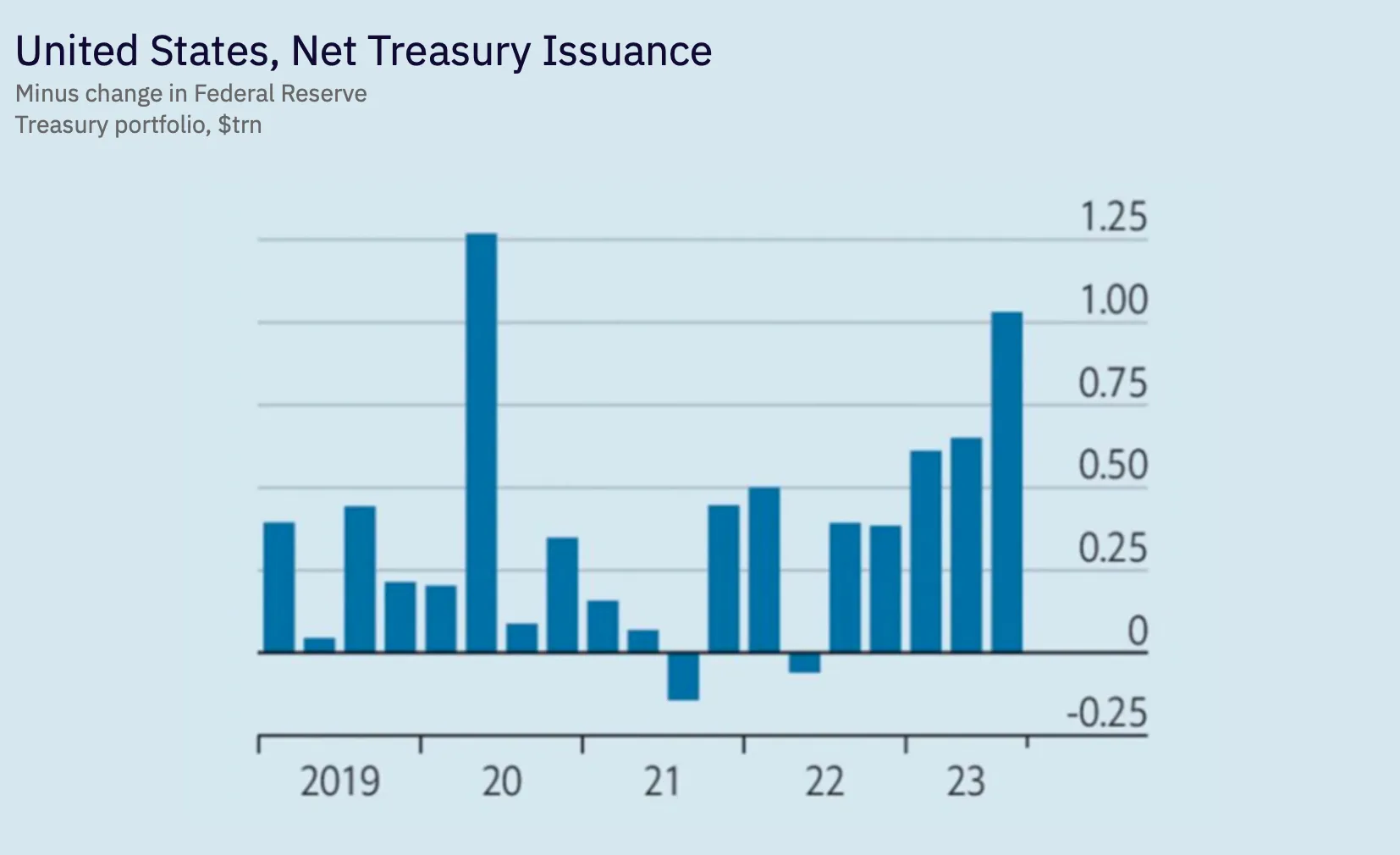

As written in The Economist, the Treasury market is one of the most important financial markets which has surged. The treasury issued $2.2trn in bills and bonds in the 12 months to October, worth 8% of US GDP to fund its deficit.

Following the FOMC meeting on December 13, 2023, the bond markets reacted notably to the Federal Reserve's decision to maintain current interest rates and signal three anticipated rate reductions in 2024.

Short-term Treasury yields, responsive to rate changes, saw a significant adjustment. The 3-month Treasury bill yield has been on an upward trend since 2022, and started the year with yields of 4.40%, reaching highs of 5.32%, a 21% increase over the course of the year.

Mid-term Treasury yields, reflecting extended borrowing costs, also experienced a substantial upward movement. The 10-year Treasury note yield climbed from 3.69% at the beginning of 2023 to highs of 4.98% throughout the year, a surge of 35%.

Similarly, long-term Treasury yields, benchmarks for the longest borrowing durations, exhibited a noteworthy elevation. The 30-year Treasury bond yield increased from 3.88% to highs of 5.11%, indicating a 32% rise.

Whilst the inversion of the yield curve has not been completely resolved, these significant yield increases across the Treasury yield curve at the longer-ends highlight the market's anticipation of lower interest rates in the near future. The Fed's communication of expected rate cuts in 2024 has led to a reassessment of investor expectations and a shift in the risk-return dynamics associated with longer-term Treasury securities.

In response to the FOMC's actions, bond investors are currently favouring shorter-term Treasury bonds, known for their heightened sensitivity to rate fluctuations. This preference for shorter maturities is expected to persist until market convictions about further rate reductions solidify.

In 2023, the global equity market witnessed considerable volatility, marked by alternating periods of strength and weakness. Nevertheless, as of early December, the market has demonstrated signs of recovery, concluding the year on a positive trajectory.

The year commenced with robust performance, as the S&P 500 exceeded $4,600 in January, closing high of $4,602.62 on January 4, 2023. However, the market encountered challenges throughout the year, including inflation reaching a 40-year peak in the US. This prompted central banks to continue to raise interest rates, heightening borrowing costs for businesses and consumers. The on-going geopolitical tensions and supply chain disruptions contributed to this volatility.

Despite these challenges, the global equity market has displayed signs of improvement at the tail end of this year. This is due to several factors, Central banks indicating a potential halt in interest rate hikes, alleviating concerns about a recession and providing support for stocks, and; strong corporate earnings which remained resilient in 2023, bolstering investor confidence despite economic challenges.

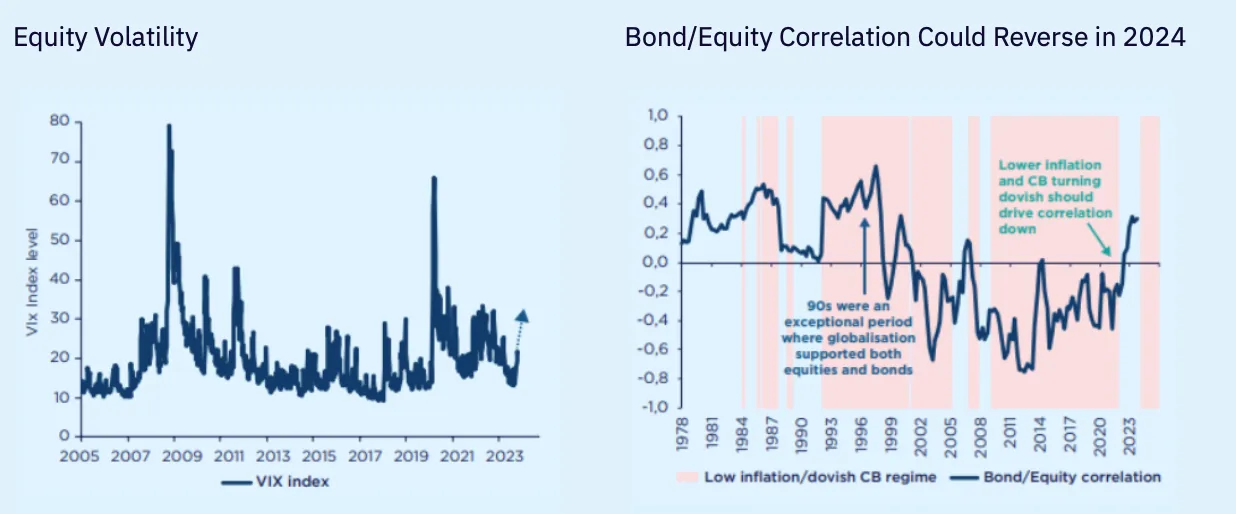

The outlook for 2024 for the global equity market presents a mixed scenario. Many pundits had firmly believed we would be in a “higher for longer” interest rate environment, based on Powell’s consistent messaging throughout the year. However, his dovish December FOMC meeting signalled three rate cuts planning for 2024. Whilst this is a positive signal for the market and many think these rate cuts are required to stop something in the system from breaking, there is the other camp who are concerned that easing of monetary policy this quickly could lead us back to a resurgence of inflation akin to the 1980’s, meaning we will have to face this pain all over again.

According to the Bloomberg US 60/40 Index, the return for 60/40 portfolios YTD in 2023 shows a return of approximately 13.8% (to 20 December 2023).Contributing to this performance are strong stock gains driven by robust earnings and economic recovery. The resilience of bond performance, offering stability amid declining yields, has acted as a hedge against stock market volatility. Diversification benefits, with stocks and bonds moving inversely, further reduced portfolio risk. The positive economic outlook in 2023, backed by lower inflation prints, has instilled investor confidence in the markets, attracting investments in 60/40 portfolios.

However, 60/40 portfolios will still face challenges with respect to high interest rates, with central banks aiming to combat inflation, putting pressure on bond yields and affecting portfolio performance, there is no certainty that rate will go back to pre-pandemic levels, or that they won’t stay “higher for longer” despite the proposed 3 cuts by the Fed in 2024. Geopolitical tensions, such as the war in Ukraine and the Middle East, have introduced market uncertainty, leading to short-term fluctuations. Additionally, technological disruptions in certain industries have impacted profitability and, consequently, the performance of 60/40 portfolios holding shares in these sectors.

Despite challenges, the portfolios have thrived on strong stock performance and diversification benefits from bonds. As 2024 approaches, investors should closely monitor rising interest rates, geopolitical tensions, and technological disruptions, adjusting their strategies accordingly.

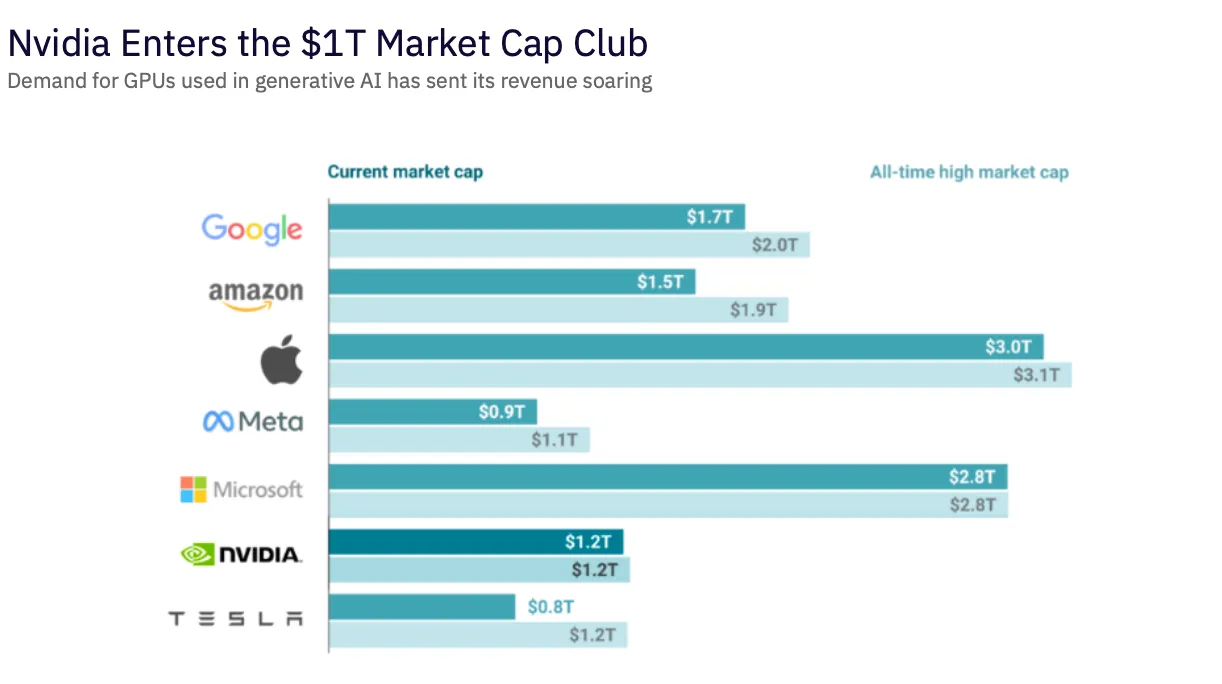

The “Magnificent Seven”

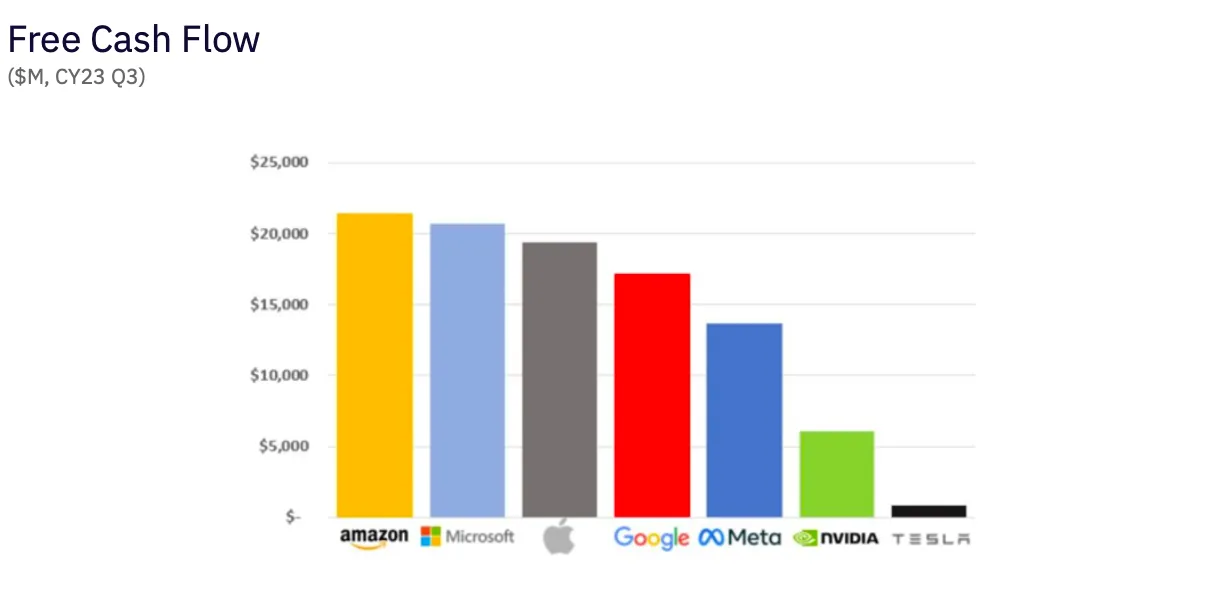

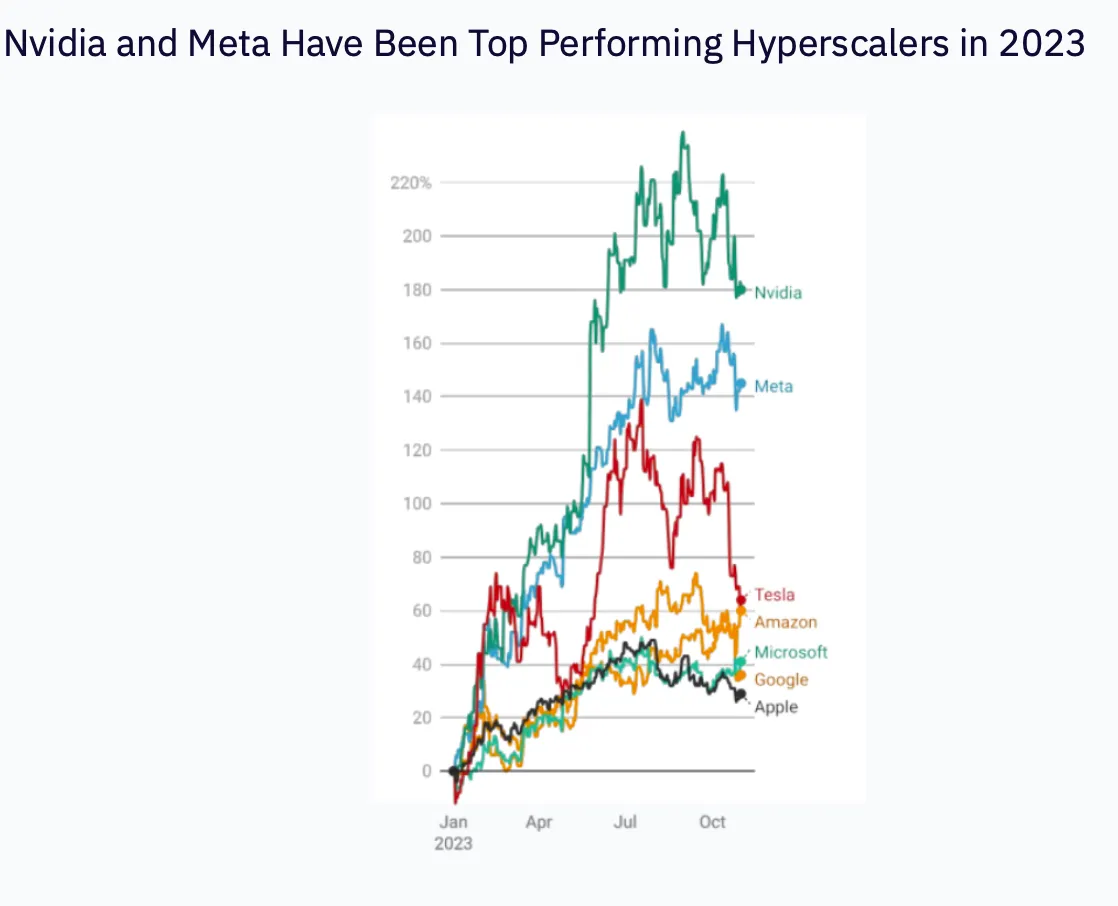

The "Magnificent Seven" tech stocks, including Apple and Microsoft, have significantly contributed to the S&P 500's impressive 23% year-to-date return. This stellar performance stems from various factors, such as consistent and robust earnings growth outpacing the broader market, strategic management of diversified revenue streams, sustained investment in innovation, providing a competitive edge in areas like artificial intelligence and cloud computing; heightened demand for products and services driven by technological advancements, changing consumer preferences, and trends such as remote work and online shopping.

The “Magnificent Seven”’s expansive global reach allows them to tap into growing economies and emerging markets, diversifying their customer base and contributing to sustained growth. Proactive engagement in stock buybacks enhances per-share earnings, increasing attractiveness to investors. Notably, the growing preference for technology stocks in the market further benefits the "Magnificent Seven," reflecting investor confidence in their resilience to economic downturns and growth potential. This convergence of factors has propelled these stocks to the forefront of the 2023 stock market, positioning them as enduring choices for investors seeking a balanced portfolio of growth and stability.

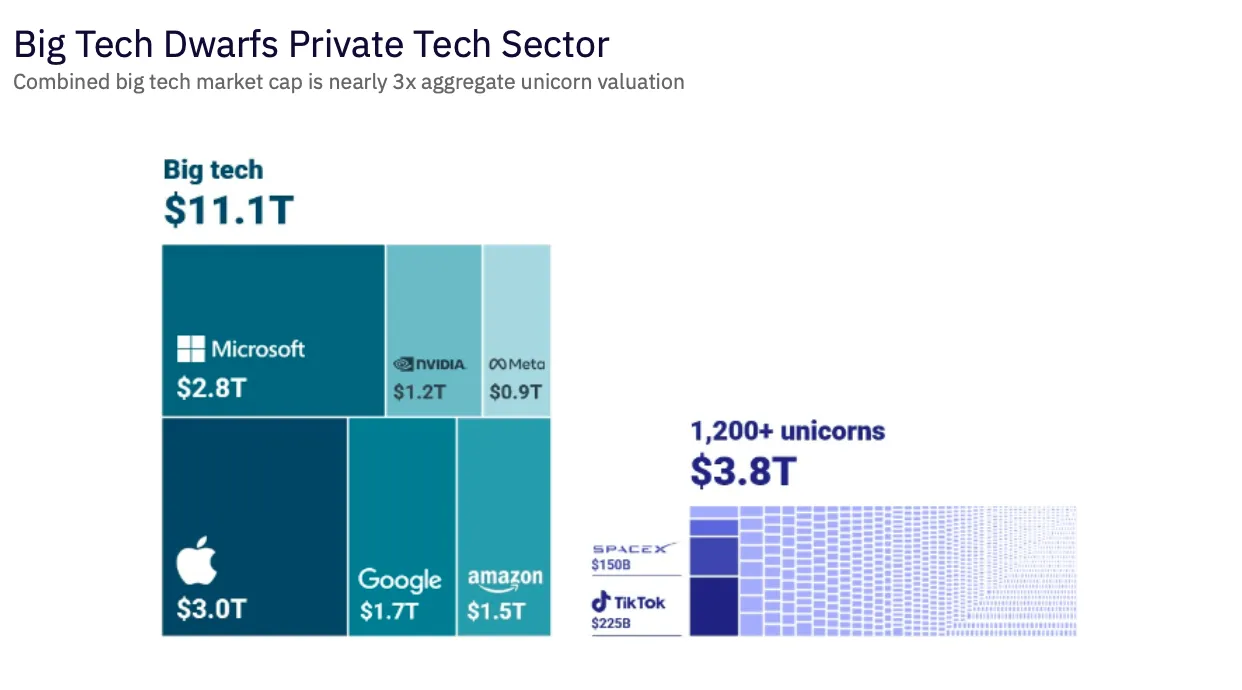

According to CB Insights data, of the Magnificent Seven, Google, Amazon, Apple, Meta, Microsoft, and Nvidia are on track to earn more than $1.65T in aggregate revenue this year.

Excluding Tesla, the six major tech companies together are worth more than £11 trillion – almost three times the value of all billion-dollar startups combined. Nvidia, a top player in making AI chips, has joined the league of major tech companies by reaching a market value of £1 trillion in Q2 2023. This significant increase suggests a major change is on the horizon, with companies eagerly adopting the game-changing possibilities of artificial intelligence.

The Asymmetrical Impact of ETFs and Indices In Individual Stock Performance

In 2023, ETFs and indices played a pivotal role in stock investment, particularly highlighted by the Magnificent Seven. Capital inflows into these funds have caused notable asymmetrical movements in specific stocks, such as the Magnificent Seven. Increased demand for passive fund investments, aiming to replicate index performance, drives the heightened capital inflow. As these funds receive additional capital, the obligation to purchase more of the underlying stocks of the index, leading to rising prices regardless of individual stock performance. Lower trading costs, linked to reduced fees in ETFs and index funds due to active management, make them prone to significant price swings during sudden capital influxes.

Leverage in certain funds exacerbates price fluctuations as they borrow funds to acquire more stocks, with leveraged ETFs showing sharper stock price increases during heightened capital inflow. Momentum investing, identifying upward-trending stocks, creates a self-reinforcing cycle. Capital flowing into ETFs tracking momentum-based indices intensifies this effect, further amplifying stock price movements. The complex interplay of passive fund investment, leverage, and momentum investing shapes the nuanced stock movements within ETFs and index funds in 2023.

Private Markets

The initial segment of this market review has offered a thorough examination of the public markets, underscoring the necessity of comprehending public market dynamics as these exert direct, knock-on influence in private market investments. Establishing a robust foundational understanding of the trends in public markets is pivotal to enable investors to derive a comprehensive insight into private market investments and their anticipated trajectory for the year 2024.

In 2023, the private markets exhibited varied performance, with certain sectors facing challenges while others thrived.

Hedge Funds

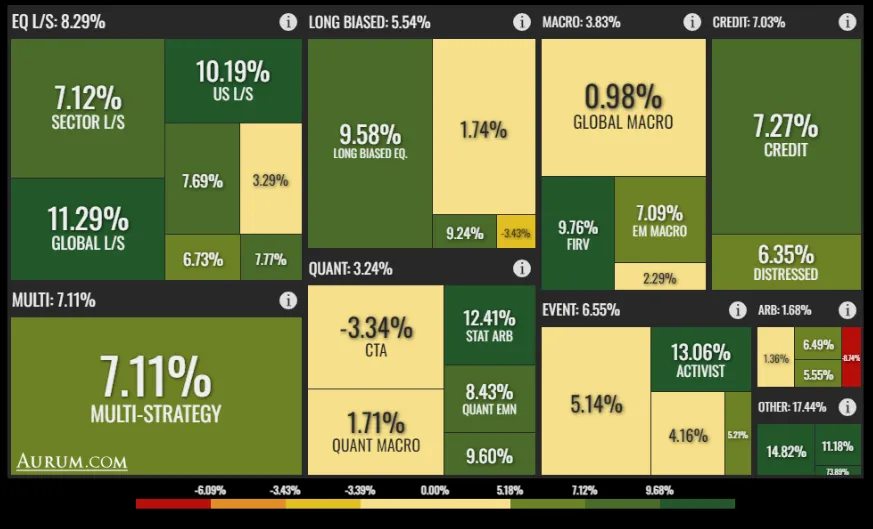

Global hedge funds contend with a challenging year, experiencing a 6.16% average return year to date, driven by factors like rising interest rates, geopolitical uncertainty, and reduced investor risk appetite. As of December 12, 2023, Hedge Fund Research Inc. (HFR) reported an average increase of 2.4% for hedge funds in 2023. Despite this overall positive trend, individual strategies exhibited considerable variation, with certain funds experiencing gains of up to 30%, while others recorded losses of as much as 15%.

The best-performing strategies in the current market landscape include the multi-strategy approach, characterised by its flexibility and the combination of long/short and market-neutral positions. This strategy has proven successful in navigating volatile markets. Credit hedge funds have also excelled, capitalising on the advantages of rising interest rates and wider spreads in corporate bonds. Additionally, event-driven strategies, particularly those focused on distressed situations and merger arbitrage, have found opportunities amidst the challenges presented by the market environment.

Private Equity

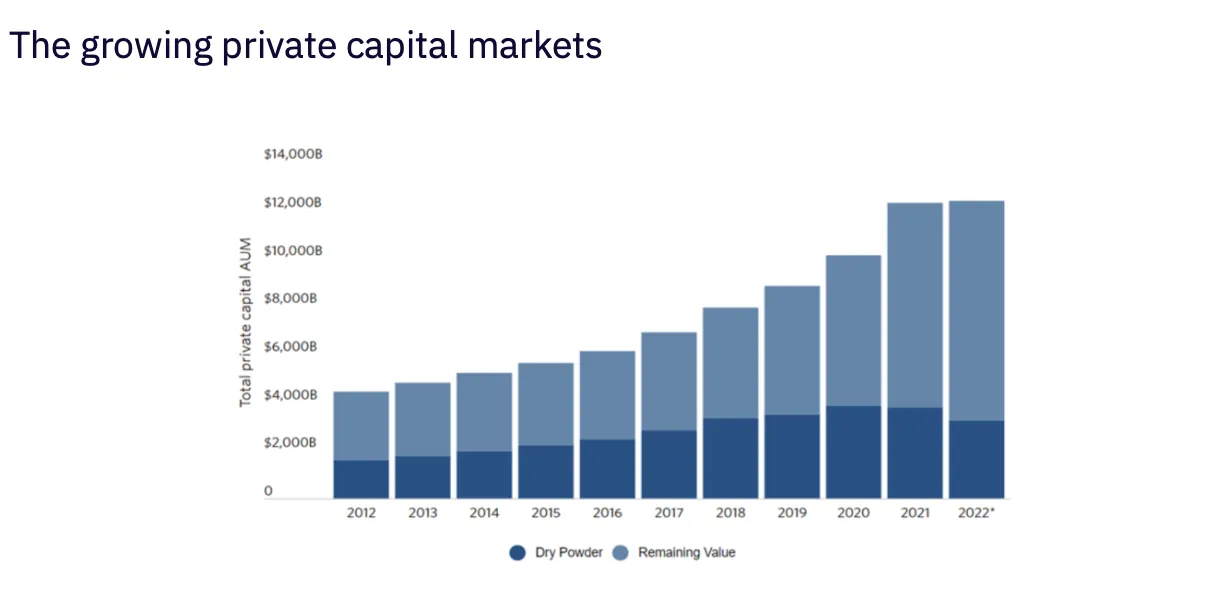

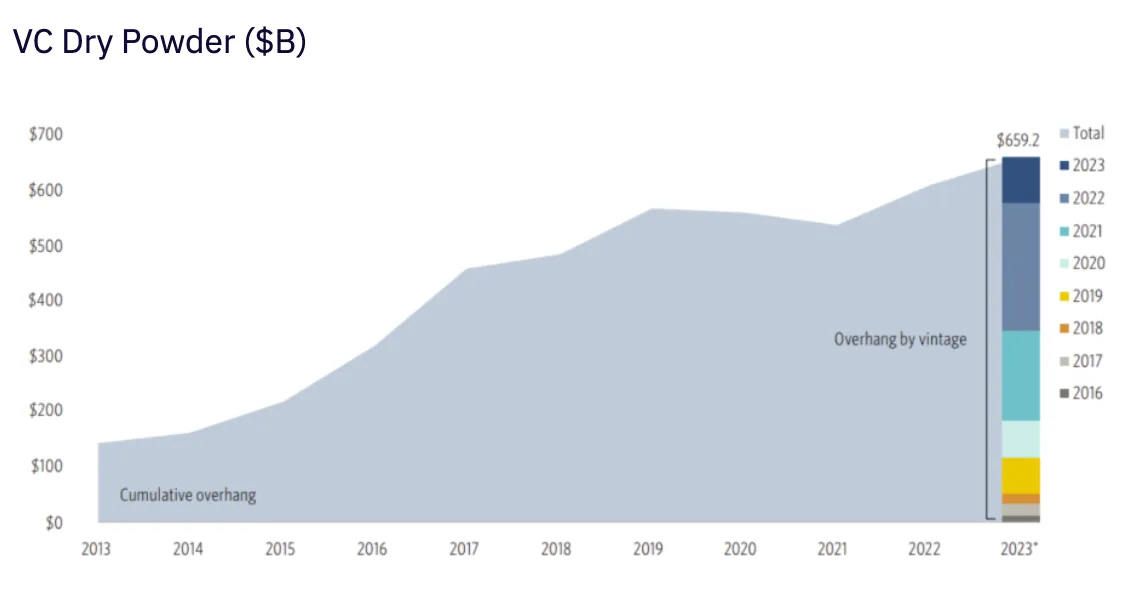

The total dry powder of the private equity market in 2023 was $2.59 trillion, up from $2.2 trillion in 2022 according to S&P Global Market Intelligence data. Despite the turbulent markets, inflows are still pouring into private equity, and this was a blockbuster year for private equity funding with CVC Capital Partners raising €26 billion for its ninth Europe/Americas private equity fund, which is the largest ever raised by a European buyout fund. The fund was oversubscribed by 2.5 times, reflecting strong investor demand for private equity investments.

Global private equity is not insulated from the heightened volatility in 2023. As reported by Preqin, the median net internal rate of return (IRR) for private equity funds in 2023 stood at 11.2%, marking a decrease from the 12.8% recorded in 2022. Notably, the performance across private equity funds exhibited considerable divergence, ranging from impressive returns exceeding 20% to certain funds incurring losses of up to 10%.

This volatility is influenced by economic outlook, underlying investment performance, and fundraising activity, however some firms have strong returns. European private equity proves more volatile than European property or infrastructure, with returns ranging from -8% to 15%. Similar factors impacting global private equity contribute to this volatility, yet specific European firms, particularly those focused on buyout investments, exhibit resilience.

Private equity performance has been affected by the tight credit spreads seen in this market environment, which poses both challenges and opportunities for private equity investments. On one hand, the increased interest rates demanded by banks are raising the cost of borrowing for private equity firms. This upward pressure on the cost of capital makes it more difficult for these firms to achieve the high returns required to attract investors.

On the flip side, the same tight credit spreads are complicating companies' efforts to raise funds through debt financing, resulting in higher interest rates on debt issuance. This situation could benefit private equity firms by potentially allowing them to acquire companies at more favourable valuations.

It is clear that tight credit spreads have a significant influence on the industry as private equity firms are grappling with increased costs for debt financing, and affecting their ability to acquire companies.

Investment selectivity is rising, with a focus on financially robust companies less vulnerable to economic downturns, and tougher negotiations on valuations indicate an awareness of companies under financial pressure, providing private equity firms with negotiating leverage.

Private Credit

The beneficiaries of the difficult financing environment have been private credit funds, which, due to their flexibility, are allocating credit where traditional investment banks can no longer step in due to their own tighter risk frameworks.

Preqin data shows private credit funds raised $168 billion in 2023, up from $145 billion in 2022. This represents a record year for private credit fundraising.

The low returns seen in bonds has driven investors to seek higher-yielding investments such as private credit, which is yielding 8% or more whilst issuing credit to companies with robust credit ratings, to provide some credit risk mitigation.

Given the recent historical correlation between the equity and bond markets, investors are looking to seek more diversification, which is driving money into private market strategies, including private credit.

Whilst private credit strategies have been successful in 2023, rising interest rates pose a threat to the net asset values (NAVs) of private credit funds, as the value of existing loans diminishes with increased interest rate demands. This is in addition to the wider geopolitical and macroeconomic uncertainty in 2024.

The Thawing of the IPO and M&A Markets

Despite the volatile market environment, IPO and M&A activity eventually began to thaw from its frozen state, with key transactions taking place, finally providing some respite to investors in private markets.

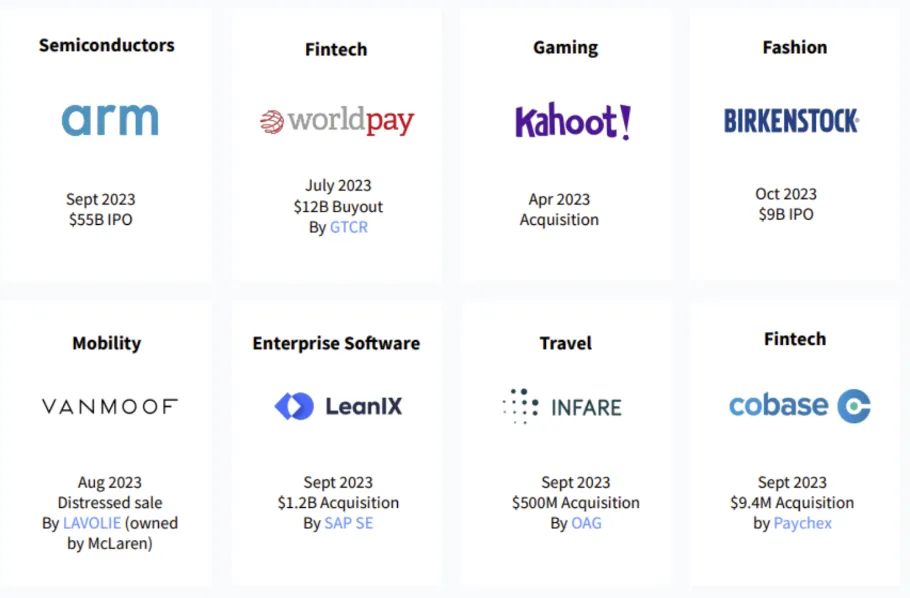

Key IPOs in 2023

- Arm Holdings Limited, a British multinational semiconductor and software design company IPO’d on the New York Stock Exchange (NYSE) on November 14, 2023 for $8.3 billion

- Birkenstock Holding Limited, a German footwear manufacturing company, IPO’d on the Frankfurt Stock Exchange (FRA) on December 6, 2023 for $7.3 billion

- ATS Corporation an American technology company that provides software solutions for the insurance industry IPO’d on the Nasdaq Stock Market (NDAQ) on April 14, 2023 for $6.2 billion

- Oddity Tech Ltd. a British technology company that develops artificial intelligence (AI)-powered software solutions for the healthcare industry IPO’d on the London Stock Exchange (LSE) on October 19, 2023 for $5.5 billion

- Klaviyo, Inc. an American cloud-based marketing automation platform that helps businesses acquire, retain, and engage customers IPO’d on the New York Stock Exchange (NYSE) on July 13, 2023 for $4.4 billion

Key M&A Transactions in 2023

- Broadcom acquired VMware for $61 billion, creating a leading provider of hybrid cloud solutions.

- Microsoft acquired Activision Blizzard for $68.7 billion, making Microsoft the third-largest gaming company by revenue.

- Telefónica acquired MasMovil for €10.9 billion, forming the largest mobile phone operator in Spain.

- GlobalFoundries acquired Tower Semiconductor for $5.4 billion creating a leading provider of specialty foundry services.

- Qualcomm acquired Nuvia for $1.4 billion giving Qualcomm access to Nuvia's ARM-based CPU technology.

The outlook for IPOs and M&A markets in 2024 reflects a nuanced landscape shaped by a confluence of factors. Optimism stems from the anticipation of a global economic recovery, propelling business growth and escalating demand for IPOs and M&A activities. This upswing is driven by companies seeking capital infusion and strategic expansion opportunities, buoyed by positive economic indicators.

The optimistic atmosphere is further reinforced by a robust investor appetite, fuelled by accumulated cash reserves over the past two years. Investors actively seek new investment avenues, aligning their strategies with the surge in IPO and M&A opportunities. The maturation of the technology ecosystem, particularly in fintech, healthcare, software and sustainability, amplifies the attractiveness of targets for M&A, contributing to the positive sentiment.

Venture Capital (VC)

KPMG's Global Venture Capital Report states global venture capital has emerged as a bright spot in the private markets industry, achieving an average return of 25%, propelled by strong demand for early-stage technology investments, successful tech IPOs, and the flourishing global tech ecosystem.

CB Insights reports the global venture capital market had $1.74 trillion of dry powder as of December 2023, up from $1.24 trillion in December 2022.

At the same time, European venture capital also shines as a bright spot in the European private markets industry, achieving an average return of around 20%, mirroring the global trend. The total dry powder of the European venture capital market was €462 billion as of Q4 2023, up from €364 billion in Q4 2022.

Whilst this has been welcomed news amidst a challenging post-pandemic environment and a stagnant exit market, the VC industry has faced ongoing difficulties; fund performance has been impacted, particularly with respect to diminishing exit opportunities since 2022 which has affected fund DPIs, ultimately constraining Limited Partners’ liquidity and capital recycling to allocate to newer fund vintages, and thus impacting VC fundraising over this period. This has led to a decline in global venture capital fundraising, totalling $117.3 billion across 955 funds in Q3 2023. Projected 2023 fundraising is expected to reach approximately $150.0 billion, the lowest since 2015, primarily due to a decrease in $1 billion-plus funds (akin to later-stage and growth funds), constituting only 16.3% of total commitments, the smallest proportion since 2015.

Economic uncertainty has posed challenges for first-time VC fund managers, reflected in a significant decline in fundraising, reaching $11.6 billion across 183 funds, the lowest since 2013 in year-to-date data for 2023. The fundraising pace is expected to remain slow in the final quarter of 2023, but an upturn in the IPO market or a decline in interest rates in 2024 could boost LP sentiment and capital influx into the VC ecosystem.

In Q3 2023, the global VC market experienced subdued performance, with a decline in both investment and deal volume, but Q3 2023 was up 5% on the previous quarter with over $81 billion invested to date according to figures published by Dealroom. The Americas led in total VC investment, driven by major raises in the United States, such as Anthropic's $4 billion and Redwood Materials' $997 million. Asia excelled in deal-making, with significant funding for GTA Semiconductor and Unway. Europe saw substantial transactions, including Verkor's $2.27 billion and H2 Green Steel's $1.63 billion raises.

Geopolitical and macroeconomic uncertainties contributed to a slowdown in global VC deal completions in Q3 2023. VC investors extended timelines, heightened scrutiny in evaluations, and prioritised existing portfolio companies. Geographic diversification was evident, with significant transactions in France, Sweden, Indonesia, Hong Kong, Australia, and Ireland. Emerging markets like the UAE, Japan, and Brazil showcased notable deals, indicating maturation in innovation hubs.

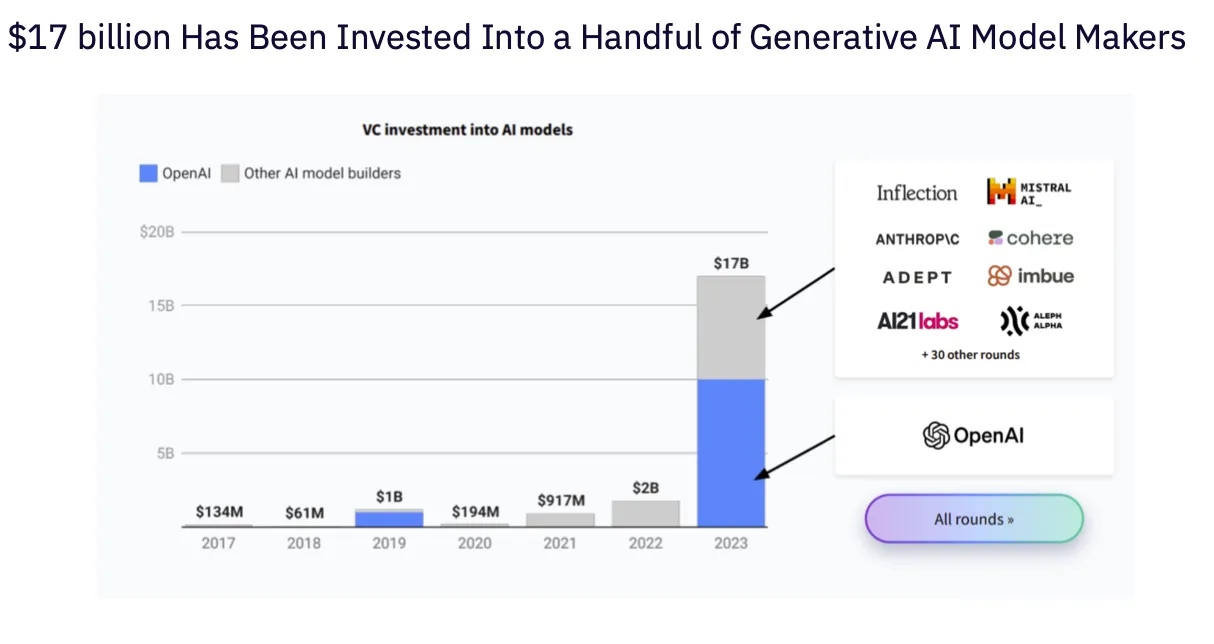

Despite cautious sentiments in global VC circles, interest surged in artificial intelligence (AI). VC investors expedited AI investments, adopting various strategies, from early-stage ventures to strategic evaluations. Q3 2023 witnessed substantial funding for AI enterprises, including Anthropic ($4 billion), Databricks ($500 million), Neuralink ($280 million), Telexistence ($170 million), and Aleph Alpha ($225 million), highlighting AI's enduring appeal as a strategic investment focus.

As we enter into 2024, it is hoped that the exit market will continue to thaw and more transactions will take place in a more stimulative wider market environment which will allow strategies such as VC to flourish again.

Despite the current difficult market environment, VC has historically established itself as a high-return investment asset class, with studies indicating an average annual return ranging from 20% to 30%. This track record underscores the attractiveness of VC to investors seeking robust returns. In addition, the VC industry has undergone significant professionalisation in recent years, marked by the presence of more experienced and sophisticated investors.

This evolution has attracted more institutional investors, including pension funds, to allocate to VC, which have been further reinforced by key policy changes, including in the UK where the “Mansion House Compact” was announced in July 2023 - an agreement which promotes nine of UK’s largest defined contribution benefit pension funds to allocate 5% of their assets into unlisted equities by 2023. The agreement's signatory members include: Aviva, Scottish Widows, L&G, Aegon, Phoenix, Nest, Smart Pension, M&G and Mercer, marking a very big move for the industry as this will provide the much needed domestic capital inflows into European VC.

Pension funds have increasingly been allocating more capital into private markets in recent years, strategically aiming to enhance portfolio diversification beyond heavy reliance on public markets. This shift responds to mounting evidence indicating heightened volatility, increased correlation, and the risk of high drawdowns in public markets. These factors have directly impacted pension funds' liability-driven investment (LDI) strategies, creating challenges in meeting immediate distribution requirements—a pressing concern for these funds. Investing in private markets enables pension funds to mitigate exposure to these risks, thereby enhancing portfolio stability and fortifying resilience against market downturns. This strategic move not only facilitates more effective pursuit of long-term investment goals but also instils greater certainty for pensioners.

The Exodus of Hedge Fund Investing in VC

During the pandemic, cash-rich hedge funds entered venture capital, boosting tech dealmaking. However, with the market downturn, many are now selling venture assets in secondary markets, usually with significant haircuts. Tiger Global, rooted in hedge funds, started the asset sale earlier this year, and others like Coatue are following suit. Whilst Tiger and Coatue adopted the use of traditional 10-year vehicles to fund start-ups, many other hedge-fund players who dabbled in VC opted for commingled structures. The challenge is even more pronounced for funds using commingled public and private vehicles, facing pressure from regular redemptions, prompting a shift away from illiquid VC strategies, causing major sell-offs.

Unlike public stocks, hedge funds lack a quick exit for private investments, leading to a surge in secondary share sales. However, these markets are still immature, posing challenges in achieving acceptable prices for the selling party, who often have to take steep haircuts. Some hedge funds, grappling with cash-flow issues, use financial engineering like loans against future sales or altering redemption rules of their funds for temporary relief.

The repercussions extend to the wider venture capital ecosystem, as large hedge fund investments were vital for late-stage startups in 2020 and 2021. Their withdrawal may impede large private companies from securing sufficient capital to stay private longer. While hedge funds are willing to cut losses in the venture class, the overall investment pace sharply dropped, with major funds participating in 436 VC deals in 2022, plunging to 76 this year—a significant 83% decline. Whilst this might cause a lack of capital injection at these stages, this may help in normalising valuations as there will now be decreased competition which had been surging prices.

The anticipation is for continued decline in hedge fund participation in venture capital through 2024 and beyond, unless rates shift to more favourable conditions.

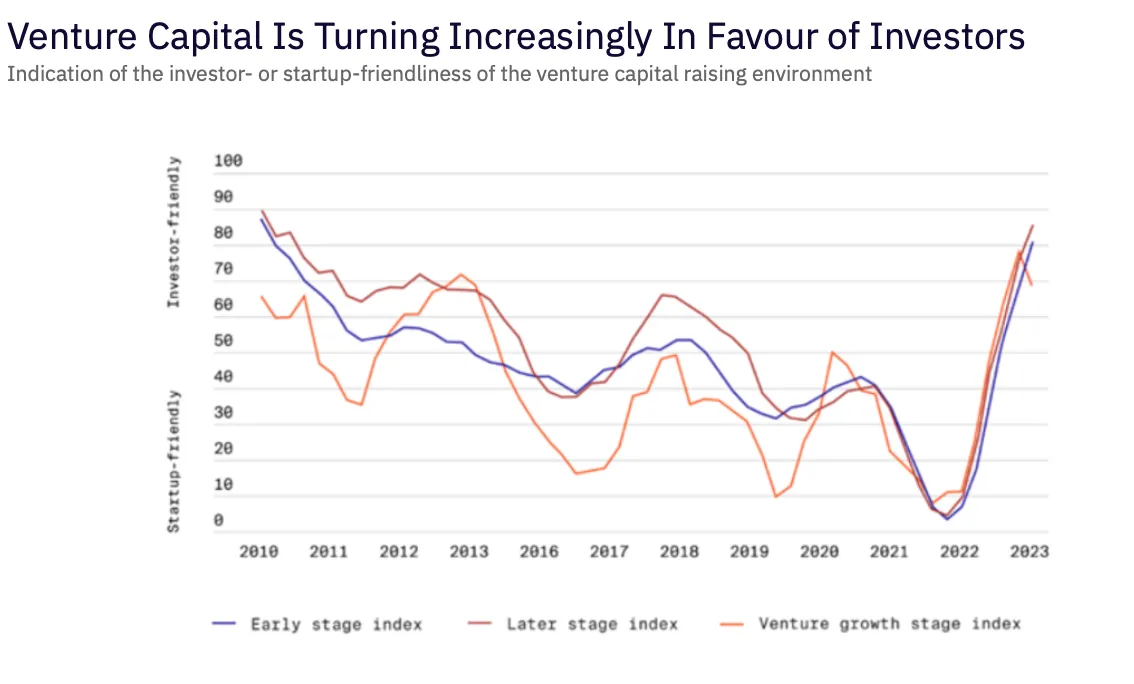

European Venture Capital

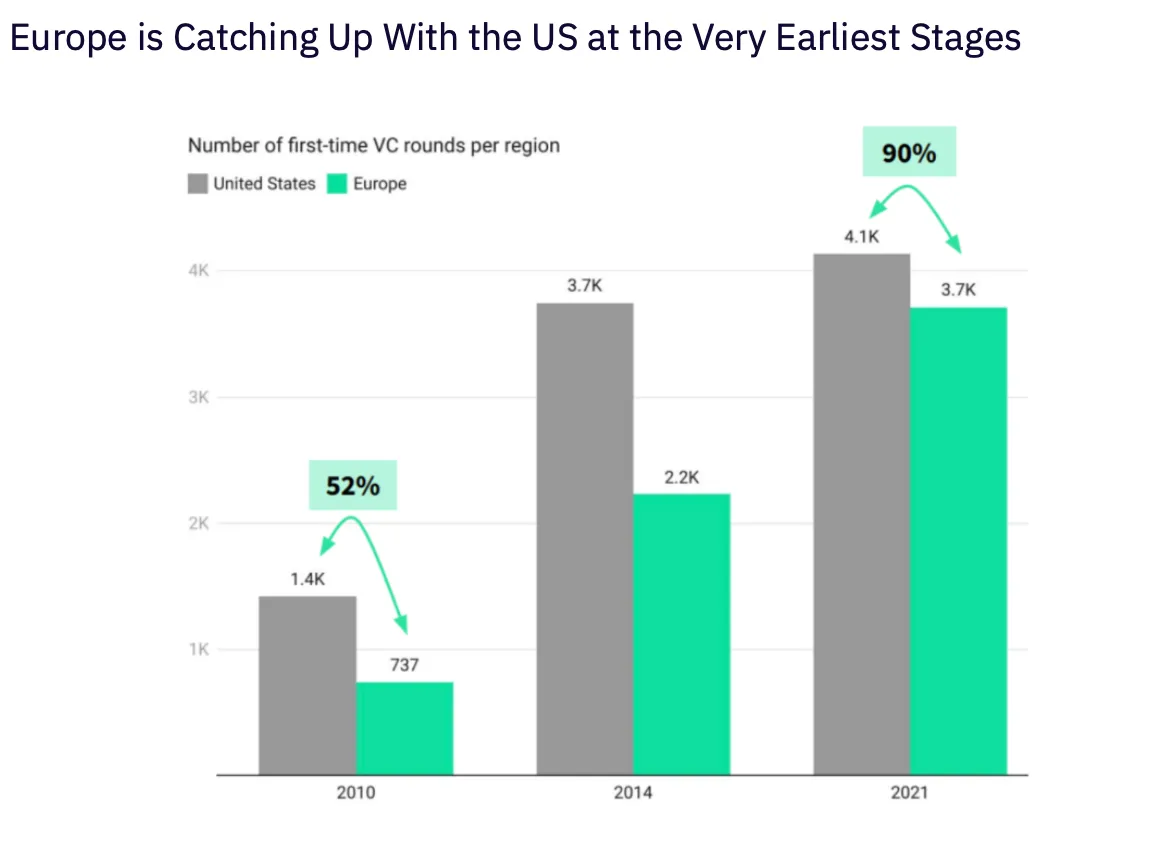

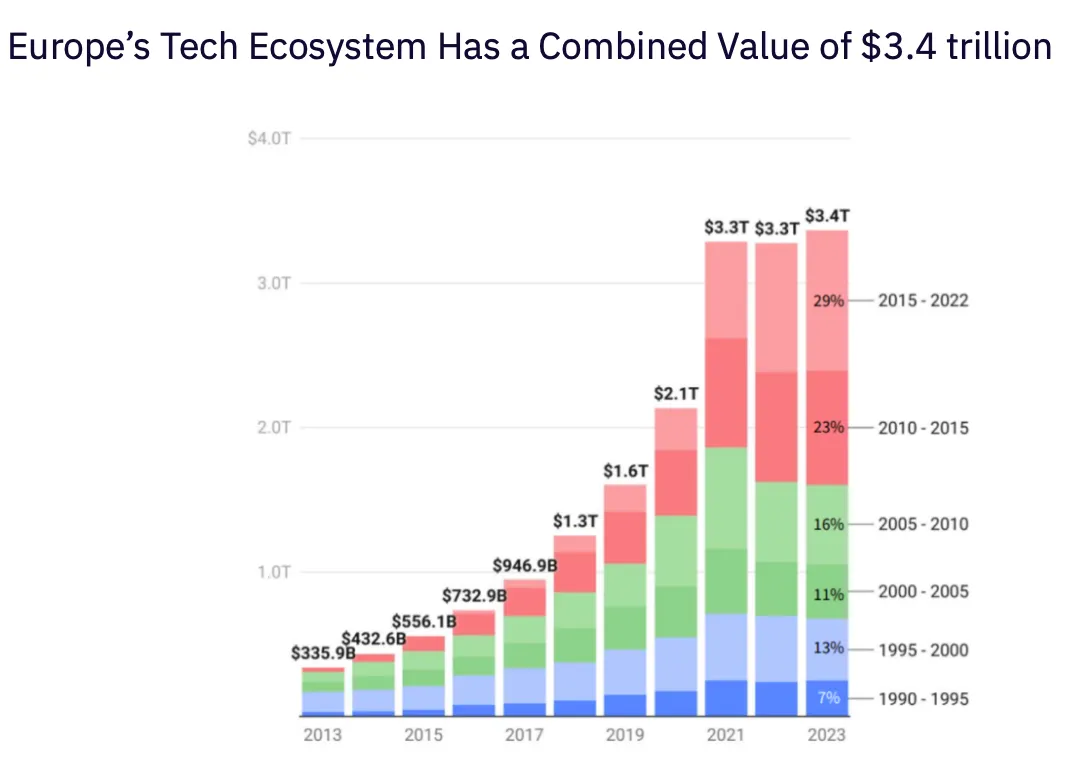

European venture capital has seen considerable maturation and statistics show it is now catching up with the US at the early-stages, the graph below showing approximately 3,700 European start-ups securing their first cheque from a European VC firm.

Data also shows the combined value of the European tech ecosystem stands at $3.4 trillion, and Europe’s share of global VC is at a record high 19%, up from 13% from 10 years ago, whilst European early-stage VC also hit a record of 24% in 2023.

Pitchbook data shows that Fintech, Healthtech, and Software claimed the spotlight as the top three most active investment areas in Europe throughout 2023. Looking ahead, the trajectory of innovation and growth appears to be steered by deep tech and frontier technologies, encompassing artificial intelligence and machine learning, robotics, and blockchain. Venture capital funds strategically positioned within these domains are poised to capture the promising upside of this technological wave.

According to the KPMG Venture Pulse report, the first nine months of 2023, European Venture Capital deal value is expected to drop by 49.1% from 2022 levels, indicating a significant decline. Despite this, activity remains comparable to pre-2021 and 2022, signalling structural growth. Short-term indicators show a 5.9% Q3 increase over Q2, hinting at a potential recovery, though uncertainties persist due to an unclear macroeconomic outlook.

The commercial services sector shows the least decline in deal value for the first three quarters of 2022. Regionally, France & Benelux gain market share, while the UK & Ireland maintain a substantial lead, contributing to 33.2% of deal value. The focus this quarter is on cleantech investment and exit activity.

Exit activity in 2023 is on track to be the most depressed since 2013. Revival hinges on broader recovery in valuations and public listings, and a wider thawing of the M&A and IPO markets. Public listing valuations remain depressed, while buyouts exhibit more resilience, with acquisitions representing the majority of exit value. Sector-wise, IT hardware is resilient, while energy experiences the greatest declines. Most top 10 exits in Q3 2023 were in the software industry.

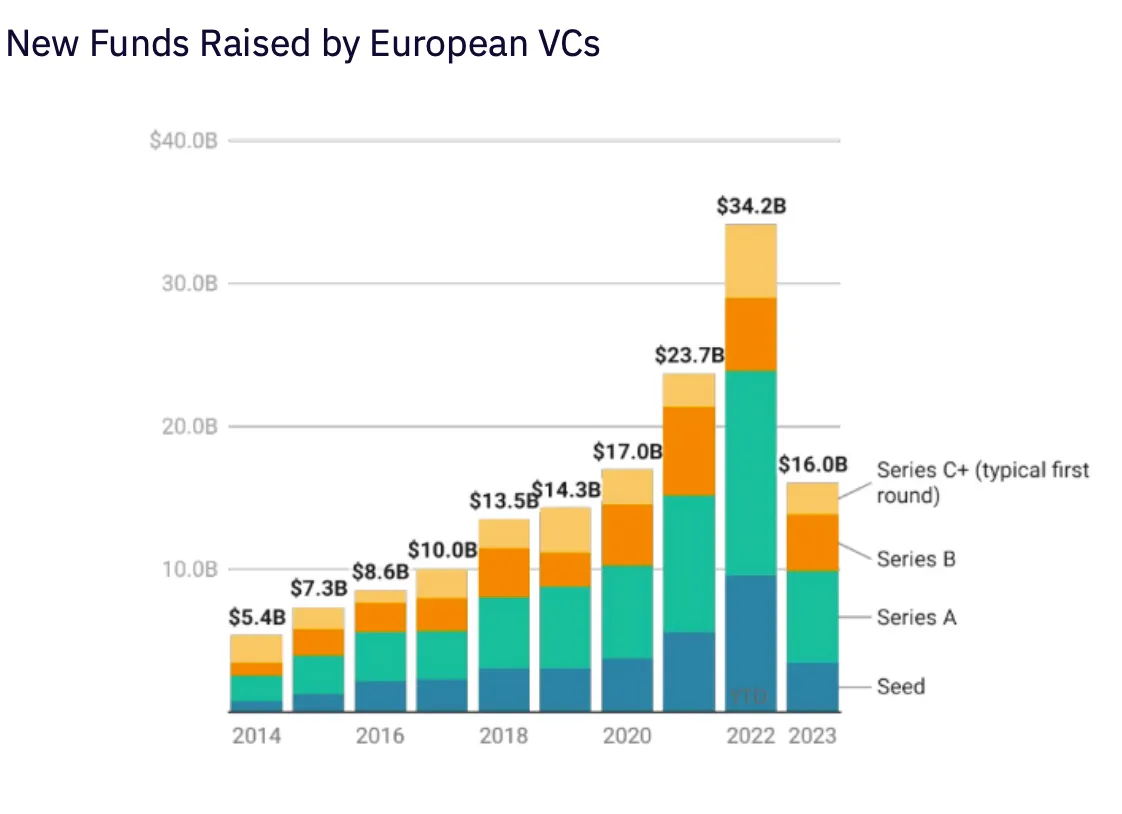

VC fundraising in Europe for Q3 2023 is half the 2022 level, at €13.9 billion over 91 vehicles. Anticipation suggests 2023 fundraising will not surpass 2022 levels. France & Benelux and DACH regions gain the most share of capital raised. The challenging fundraising environment is evident, with median fund closing times at 15.1 months in 2023, up from 9.0 months in 2022. A shift towards more experienced managers is observed.

Venture deal activity reveals a 49.1% decline in deal value for 2023 from 2022. Signs of potential recovery emerge, with deal value increasing since Q1 2023. Early-stage VC trends upward from Q1 2023, with cleantech and AI technologies prevalent. Top 10 deals in Q3 2023 lean towards cleantech investments. France secures the largest deal at €2.1 billion for Verkor, and Sweden attracts a €1.5 billion investment in H2 Green Steel. Commercial services and France & Benelux show the most resilience. Despite challenges, France & Benelux comprise 23.2% of deal value in Europe through Q3 2023. The proportion of US investors in Europe has declined, potentially due to increased focus on domestic investments amid market uncertainty.

Findings published in Pitchbook’s Q3 2023 European Venture Report and data published in Orrick’s European Venture Capital Deal Term Review 2022, Crunchbase and Dealroom show the fervour of 2021 and early 2022, marked by Series A average deal sizes of €40 million and €43-45m respectively, and average valuations of €200m and €250m respectively have significantly subsided. In Q3 2023 the average valuation of companies was €225m (partly bolstered by the surge of large AI deals) with an average deal size of €37.5m. This decline, particularly with respect to average deal sizes, from the peaks of 2021-2022, are more aligned with the numbers seen in 2020, with average valuations of €150m and an average deal size of €36m. They also align with the current broader economic uncertainties, including concerns around inflation, geopolitical tensions, and the potential for a recession, whilst still signalling structural growth without the froth. This is particularly important in an environment in which investors demand stronger financial performance and a clearer path to profitability from early-stage companies, and has been viewed positively as a healthy development from the exuberance of 2021.

The shift in valuation patterns may temper excitement surrounding early-stage startups but signals a return to a more realistic landscape, fostering a sustainable and balanced ecosystem. In the wider VC landscape, Europe's AI sector experienced a surge in Q3 2023, raising $1.8 billion, representing 11% of the continent's total funding for the quarter and close to one-fifth of global AI funding. Notable AI companies, including Builder.ai, Quantexa, Synthesia, and Aleph Alpha, raised significant funding. This underscores the growing maturity and potential of the European AI sector, positioning Europe to play a leading role in driving AI innovation.

Notable VC deals in 2023:

- OpenAI, currently valued at between $80-90 billion, raised over $300 million in funding from firms such as Sequoia Capital, Andreessen Horowitz, Thrive and K2 Global at a valuation of $29 billion. It also secured a separate investment from Microsoft in January 2023, believed to be around $10bn.

- Mistral raised €385 million in Series A funding with a valuation of $2 billion from investors including: Andreessen Horowitz, Index Ventures, Accel, Eurazeo and Softbank.

- Aleph Alpha raised €500 million in a Series A funding, valuing the company at €4.1 billion. Investors included: Bosch Ventures, Caisse de dépôt et placement du Québec (CDPQ), Deutsche Telekom, EQT Ventures, HSBC Trinkaus, Intel Capital.

OpenOcean remains committed to our mission in empowering the bold leaders of the data economy by investing in companies that are developing solutions to the world's most pressing challenges, and which are disrupting traditional industries which are likely to challenge the status quo and to create new opportunities for growth. Our focus has always been on companies which are building the infrastructure of the future which will play a critical role in shaping the way we live, work, and interact with the world around us. We firmly believe Europe is poised to generate the leaders of tomorrow, and the opportunity to back these companies is now.

We are acutely aware that it is within these market environments, the next game-changing winners of the future are born, after all, diamonds are created under pressure, and historical data has shown us that companies which are able to survive in this market environment, are set to be the leaders of tomorrow when markets return to more favourable conditions.

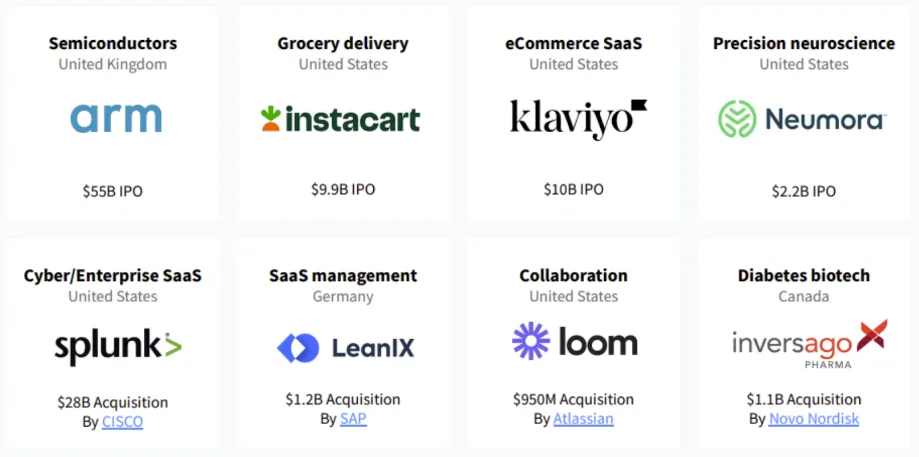

Below are just some of the examples which cover the winners from the Great Financial Crisis of 2008.

In spite of the turbulent year, OpenOcean has been committed to our proven investment strategy, and we have seen positive developments within our portfolio throughout the year, including:

- Hygraph successfully raised $30m Series B funding in March 2023, led by One Peak

- Binalyze secured $19m Series A funding led by Molten

- MindsDB secured $16.5m of funding from Benchmark in February 2023, with a subsequent $25m funding led by Mayfield in June 2023

We are also pleased to announce that many companies in our wider portfolio, including Booksy and Supermetrics, have continued to grow despite the challenging market conditions, showing their resilience and market demand for their products and services.

In addition, the surge in demand and adoption of AI and big tech by corporates and wider businesses in the past year has been a positive development for many of our portfolio companies, including IQM, one of the leading Quantum Computing companies in Europe, and LatticeFlow, a technology company from Switzerland which improves AI model performance and safety specifically by auto-diagnosing and helping to address issues with underlying data resulting in more trustworthy and performant AI models.

Whilst corporate balance sheets have been squeezed, businesses have been focused on implementing tools to increase productivity and automation, another positive development for our portfolio companies such as Workfellow and Operations1.

As homage to our open-source roots, OpenOcean successfully collaborated with Oxford University to deliver an open-access project, the O3 platform.

The O3 platform was successfully launched at the CogX festival in September 2023 and aims to bring transparency to the venture ecosystem through a unique O3 taxonomy, co-developed by Oxford and OpenOcean. This taxonomy covers business models, technology, investors, and founding teams with unprecedented granularity, facilitating exploration through the open-access O3 web tool.

Led by Oxford University's Professor Mari Sako and Dr Matthias Qian, and OpenOcean’s Ekaterina Almasque and Ollie Sellers, this collaboration provides OpenOcean with access to proprietary datasets and research, enhancing the quality of available data and offering a competitive edge in identifying unparalleled investment opportunities. The O3 initiative focuses initially on Artificial Intelligence in the UK, utilising an AI-powered platform to create the most granular map of the tech startup ecosystem. Media outlets have recognised it as the "World's most accurate" startup data platform, highlighting its potential to identify gaps in the AI ecosystem.

With this we conclude our annual macro and market update. We hope that you found this informative and that our holistic summary of the ever-evolving developments of the macroeconomic picture and its impact on the public and private markets may help to highlight areas which you may wish to investigate further with respect to your own portfolio. We very much welcome conversations on any of the topics covered within this update.

With our best wishes,

The OpenOcean team

Legal Disclaimer

The information contained has been prepared from original sources and data we believe to be reliable. Furthermore, it contains statements that are not purely historical in nature but are “forward-looking statements.” These include, among other things, projections, hypothetical analyses of income, yield or return and future performance targets. These forward-looking statements are based upon certain assumptions, not all of which are described herein. Actual events may differ materially from those assumed. All forward-looking statements included are based on information available on the date of this presentation material and there can be no assurance that estimated returns or projections can be realised, that forward-looking statements will prove to be accurate or that actual returns or results will not be materially lower than those presented. Therefore, undue reliance should not be placed on such forward-looking statements, and nothing contained herein is, or should be relied upon as, a promise or representation as to the future performance of investment.

In considering any prior performance information contained herein, prospective investors should bear in mind that prior performance is not necessarily indicative of future results. Prospective investors are encouraged to contact representatives of OpenOcean to discuss the procedures and methodologies used to calculate the investment performance information provided. Actual realised proceeds on unrealised investments will depend on, among other factors, future operating results, the value of the assets and market conditions at the time of disposition, any related transaction costs and the timing and manner of sale, all of which may differ from the assumptions on which the valuations reflected in the historical investment performance data contained herein are based. Accordingly, the actual realised proceeds on such unrealised investments may differ materially from the returns indicated herein.

OpenOcean makes no representations or warranty as to accuracy, completeness or reliability of the information contained herein (or as the case may be, the reasonableness of the assumptions on which they are based) and undertakes no obligation to update this document or to correct any inaccuracies therein.