At OpenOcean, we’ve long believed in automation software’s potential. It’s been a core theme in our investment focus for years, giving us early and continued exposure to exciting developments in the field. In the past years we’ve also shared our insights externally through our Intelligent Enterprise Automation Map, the most comprehensive overview of companies and funding in the enterprise automation space.

Preparing this year’s update revealed a clear shift as generative AI has fundamentally reshaped the landscape. With enterprises eager to unlock real business value from GenAI, automation has risen to a new spotlight as it’s one of the most immediate and tangible ways to drive measurable value out of this new technology. As a result, virtually every enterprise product now positions itself, at least partly, as automation software.

Automation software is clearly living its renaissance. But while we’ve made indisputable advances in the underlying automation technologies, many of the original challenges remain. Achieving consistent, measurable ROI from automation software is still far from straightforward. We wanted to take a moment to share our perspective on the current status of enterprise automation and the potential of the post-GenAI automation software landscape.

Foundational models spearheading the investments

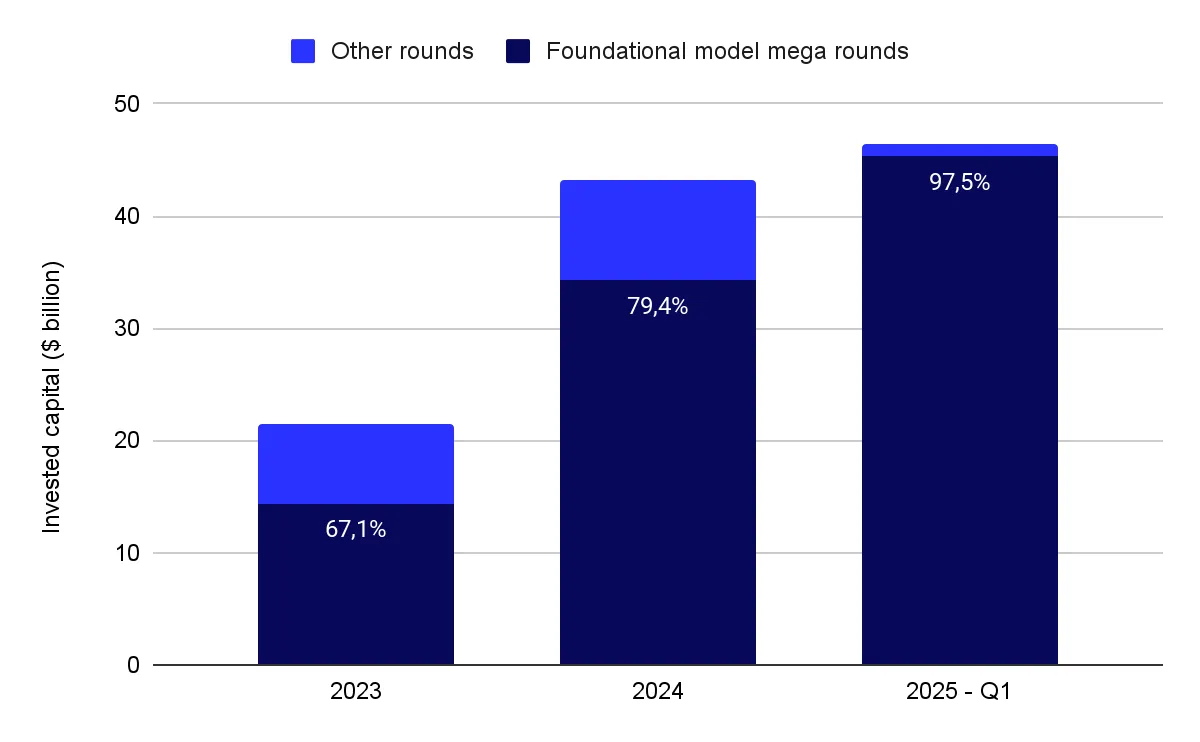

Automation investment saw a sharp increase in 2024, after a relatively calm year of 2023. Over $41.5 billion was invested, more than double the previous year. Most of the capital, however, flowed not into application-layer automation tools, but into foundational AI model companies building the core infrastructure behind the GenAI automation wave. OpenAI, xAI, Anthropic, Moonshot, Baichuan, Mistral, MiniMax, and Perplexity together received more than 75% of all automation-related funding. However, even when excluding these outsized rounds, the sector still saw healthy growth. Automation software outside of these major foundational model funding rounds saw a 26% increase in funding, rising from $7.1 billion in 2023 to $8.9 billion in 2024.

Early figures from 2025 suggest further acceleration. In the first quarter alone, over $46.5 billion was raised in the automation sector. While OpenAI’s $40 billion round in March highly skews this trend, it’s clear that both investors and enterprises maintain strong interest. For example, Goldman Sachs projects global AI investment to reach $200 billion by the end of 2025.

A persistent execution gap

Looking ahead to the potential of post Gen AI automation, modern AI-powered automation faces the same challenge as its predecessors: despite strong investments, many organizations struggle with realising true value and return on investment from automation initiatives. There is still a significant gap between automation's expected and delivered value. For example, research by McKinsey suggests that digital transformation efforts typically achieve less than one-third of their projected impact.

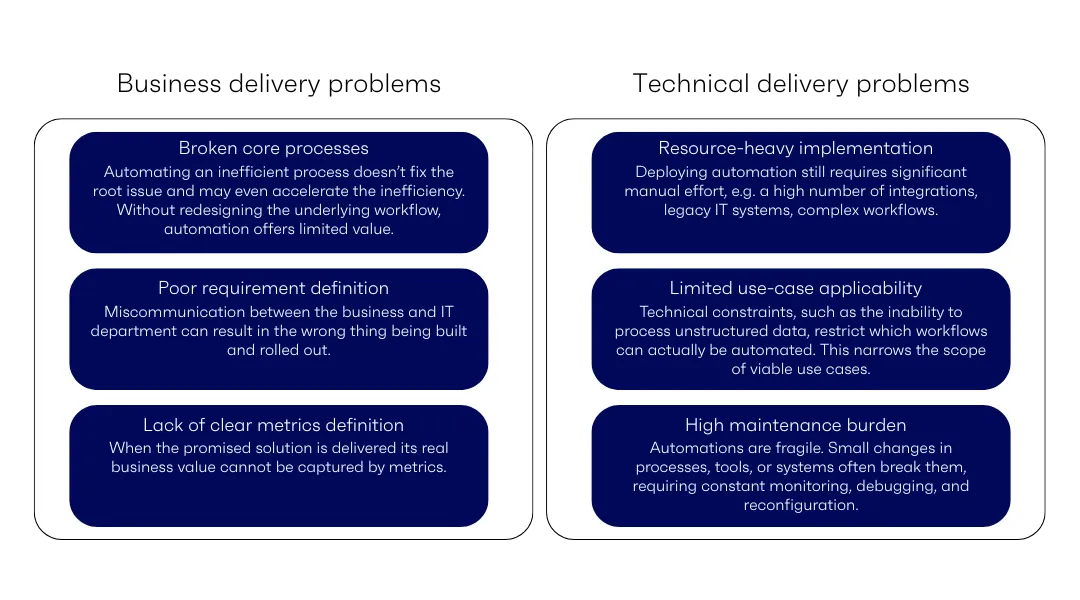

The core reason lies in the nature of automation itself: automating human work is inherently not solely a technical problem but an organisational one. Projects typically span multiple teams and processes facing challenges from misaligned goals to unclear process definitions. On the other hand, earlier tools, like traditional RPA platforms, have struggled to meet the demands of real-world environments, falling short in handling the dynamic, context-rich tasks that humans perform daily.

The automation projects' value creation problems can be categorised as follows:

Due to this multifacetedness, a high portion of automation’s current value creation is not captured mainly by software companies, but rather by service providers. Setting up automation in the enterprise context is a complex process requiring strong expertise on both the business and technical side, and most enterprises don’t have these resources in-house. As a result, external consultants and implementation partners often do the heavy lifting and, in turn, capture the bulk of the project’s value. This can be illustrated by looking at an example from the RPA space: for every dollar UiPath earns, an estimated $7 flows to service providers like EY for implementation and consulting support.

GenAI is not a silver bullet for all automation challenges

Given this context, it’s clear that while the emergence of foundational GenAI models has skyrocketed our expectations for automation, it doesn’t automatically lead to greater value creation. Instead, the true potential of AI-driven automation lies not in the technology alone, but also in its ability to bridge the gap between our expectations and delivery.

Taking a closer look at GenAI’s value in automation, its impact can be divided into two key areas: (1) expanding the range of tasks that can be automated, and (2) introducing a new agentic architecture that enables more autonomous and intelligent workflows.

- Expanded use cases

GenAI unlocks automation for tasks that involve unstructured data, synthesis, search, and content generation. These capabilities underpin much of modern knowledge work, enabling automation in areas that have historically been difficult to address, such as for instance legal services, software development, and research.

- New architectures

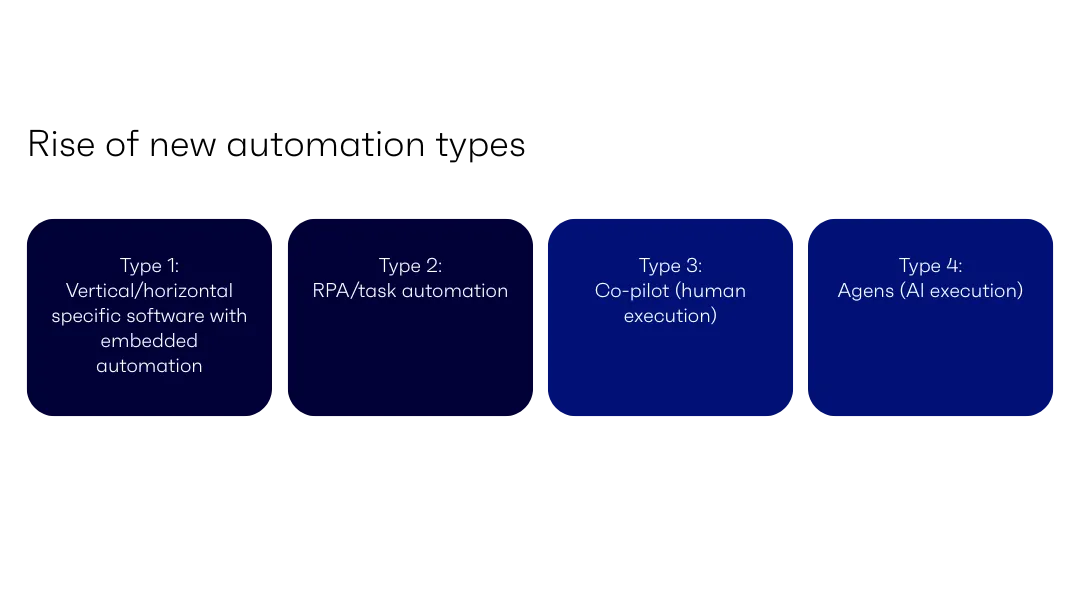

Traditional automation systems could be categorised into embedded process flows or RPA-style task automation. GenAI enables more flexible formats, including:

- Co-pilots: tools that augment human workflows in real time

- Agentic AI: systems capable of autonomously executing entire processes

The promise of new AI agentic architectures lies in their dynamic and adaptive nature. Traditional automation software attempted to model complex real-life processes with rigid rule-based systems, which often struggled in real-world enterprise environments involving multiple stakeholders and rapidly evolving requirements. In contrast, new cognitive agentic architectures can dynamically automate end-to-end processes, performing complex multi-step tasks independently and automatically adapting to uncertainties, such as new data formats.

GenAI’s role in value creation

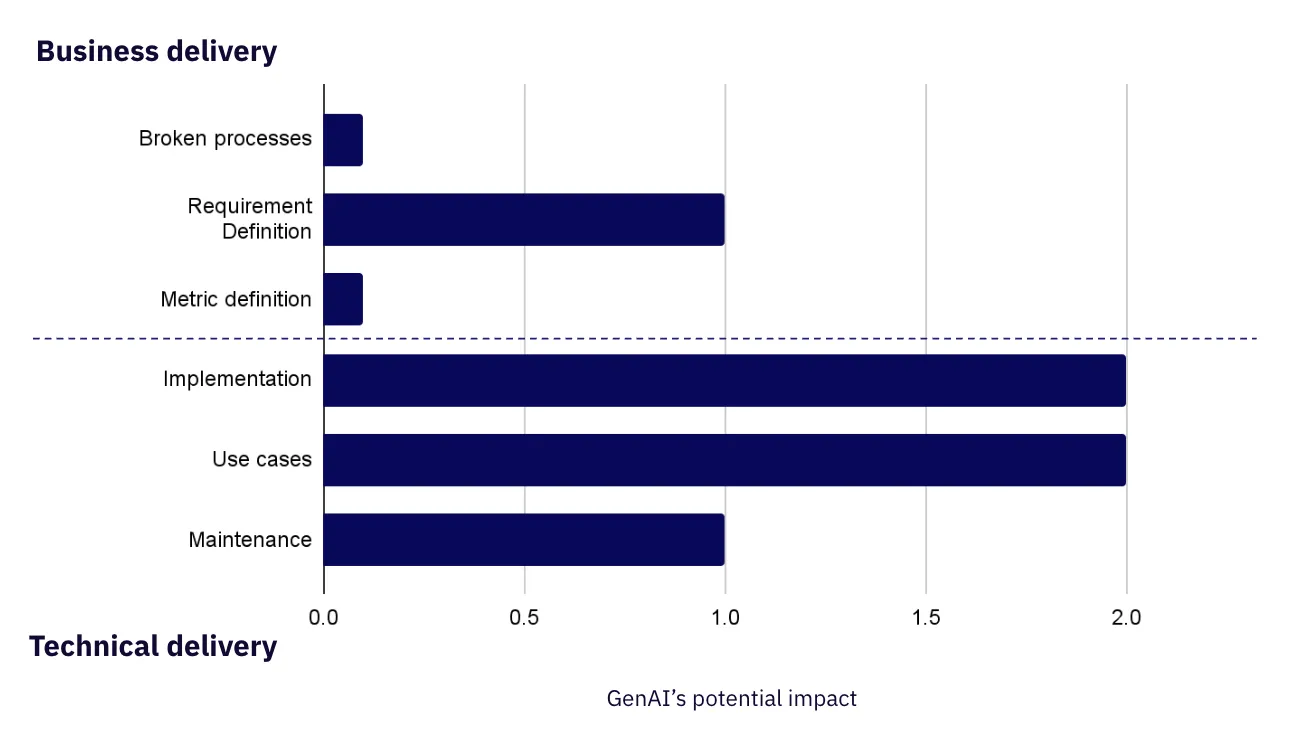

Reflecting on these changes againts the challenges of value creation in automation, it’s clear that GenAI holds significant promise in the technical delivery side. It allows automation to take over previously impossible tasks, unlocking higher-value use cases and dramatically broadening the scope of automation applications. Additionally, it has lowered development and maintenance costs by removing the need for hardcoded exception handling.

On the maintenance side, the dynamic architecture of agentic systems can reduce the need for constant manual intervention when new edge cases arise. However, the increased complexity of these systems also introduces new management challenges. We may transition from “spaghetti code” to “spaghetti agentic systems”, where multiple independent systems work toward a common goal with limited visibility into how these workflows interact and operate together.

However, the impact of GenAI on the business delivery side is more nuanced. Some improvements may come from more accessible tools. Agentic systems are beginning to enable prompt-based interfaces and low-code workflow design, bringing more users into the design and development of the solutions. This could allow business users to take greater ownership of automation, reducing reliance on specialist technical teams. However, many of the dynamics on the business delivery side are likely to stay the same. If the underlying business process is flawed, it does not much matter how intelligent the automation workflow is. In fact, more advanced automation can even worsen inefficiency. Early findings from McKinsey suggest that many companies adopting GenAI are realizing that they need to redesign their workflows entirely to unlock its true value.

The role of services is unlikely to decline, as service-led value capture continues to dominate. For example, in Q1 2025, Accenture reported $4.68 billion in annualised revenue from GenAI-related work—more than OpenAI’s total revenue for all of 2024, which stood at $3.8 billion.

Where we see opportunity to invest

The most promising automation businesses align delivery with impact. Given the technical complexity and organisational challenges involved, few enterprises are positioned to succeed without support.

Our investment focus is on the following areas:

- End-to-end AI platforms at specific verticals: – Full-stack platforms delivering “out of the box ready to use” solutions in the verticals such as HR, legal, finance & health that require little to no integrations and onboarding.

- AI-enabled services – Hybrid models that combine software with embedded services, helping customers extract value faster by pairing automation technology with hands-on delivery.

- Tools enabling enterprises to adopt AI automation – Infrastructure and developer tools that help teams integrate and manage GenAI-powered automation across workflows, securely and at scale.

If you are building in those spaces, we’d love to hear from you!