Last November, we laid out a vision for AI-native services: businesses rebuilt from the ground up to combine the margins of software with the resilience and depth of services markets. Since then, we have taken dozens of first meetings, explored more than 15 verticals, backed our first deals, and sharpened our thesis along the way.

At the core is our belief that the Age of AI is bringing about a structural shift in how services are built and delivered.

Here is what we have learned and how we are thinking about the opportunity now.

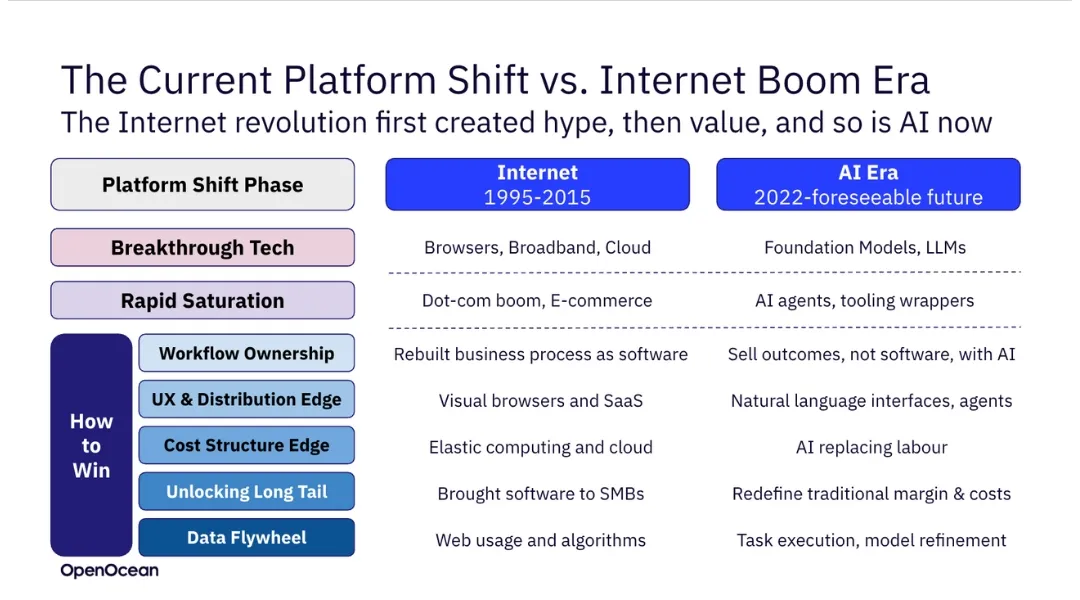

A platform shift, not a passing trend

Every major technology wave follows the same arc: breakthrough, saturation, then sustained value creation. The internet followed that arc. AI will too. But where software reshaped white-collar workflows via the browser and cloud, AI changes something deeper. This time, the unit of change is not the interface — it is the labour.

AI-enabled services are not about selling software to humans. They are about replacing or amplifying humans inside the workflow. That is a profound shift, and it is where the next category-defining companies will emerge.

What hasn’t changed: the fundamentals of venture

The stack is changing, but the rules of venture remain consistent:

- Outcomes, not tools, win markets. Clients pay for results, not code.

- Defensibility still matters, and data + distribution are the new moats.

- Power laws still drive returns. The right bet matters more than the number of bets.

- Disruption beats augmentation. New entrants win when they rethink service delivery from first principles.

And here is the kicker: for two decades, we have been chasing software’s five per cent share of global services spend. What about the remaining 95 per cent?

Where we’re focusing: a new playbook for services

Across the verticals we have assessed, the best opportunities share five attributes:

- Large, fragmented markets with low-NPS incumbents

- Repetitive, human-intensive work under cost pressure

- Workflow structures that are automatable

- Founders with both operational and product DNA

- Clear, measurable AI value creation is visible in the P&L

We use a four-part framework to assess each opportunity: Market, AI Value Creation, Team, and Growth Model. When all four align, we lean in.

One model, many entry points: software, services or both

There is no single starting point for building an AI-native services business, but there is a clear trajectory.

Some begin by building vertical SaaS tools for incumbent service providers. This vSaaS-first approach helps them embed into workflows, build proprietary datasets and gain traction. Many of these businesses later evolve into full-stack service providers. Why? Because delivering the service unlocks better margins, stronger feedback loops, and more defensibility. You move from selling the shovel to mining the gold.

Others skip the SaaS wedge and go directly to building or acquiring AI-native services businesses, either de novo, from scratch, or inorganically, through M&A. The choice depends on the vertical. Acquisition is often faster in regulated or standardised industries such as insurance or inspections. Building ground up can outperform in fragmented and fast-moving markets like recruitment or marketing.

As these businesses scale, another layer opens: franchise-style growth. Once a company has built internal tooling and proven playbooks, it can license its stack to other operators, offering infrastructure, taking a share of revenue, and turning challengers into platforms.

This evolution, from software to full-stack to ecosystem, is already evident in our pipeline and portfolio.

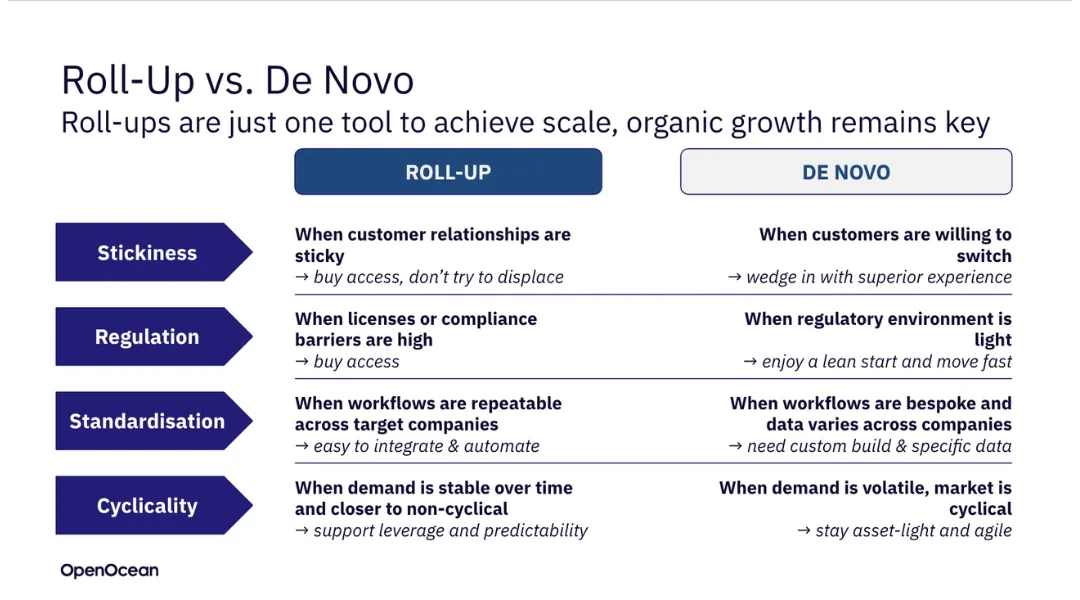

Roll-up or De Novo? It depends

Not all markets are created equal. In some, high regulatory or relationship-based barriers make acquisitions the fastest path to entry. In others, workflows are bespoke, switching costs are low, and a wedge product can outperform incumbents from day one.

We are agnostic to method. What matters is the match between strategy and market:

- Roll-ups win in sticky, regulated, standardised, and non-cyclical verticals.

- De novo works best in agile, lightly regulated, fragmented, and volatile ones.

We have seen and, and in some cases, backed both models in practice. Sometimes the most effective approach blends the two: starting with one to gain initial traction, then complementing it with the other as the company scales.

What makes the model work

At their best, AI-native services businesses deliver three core value drivers:

- Margin expansion: Automating repetitive work reduces cost and scales delivery

- Revenue acceleration: Better service drives retention and pricing power

- Platform potential: Proprietary data and tooling create long-term leverage

This is how AI-enabled services evolve from “agency with AI” to full-stack vertical platforms. And it’s how they earn higher multiples at exit—even when valued on EBITDA, not revenue.

What we’ve backed and what we’re exploring

Over the past six months, we have backed a few companies across Europe that fit this model. Some are pre-operational. Others already have traction. In each case, we have underwritten based on the framework above.

We have also identified a set of verticals that consistently score high across our criteria (AI leverage, revenue quality, fragmentation, right to win):

- Property management

- Clinic services and healthcare

- Insurance brokerage

- Compliance and KYC services

- Debt collection

- Testing and inspection

- Customs brokerage

These are verticals where incumbents are asleep or constrained, and where AI-native challengers can build a durable edge.

Where we’re headed next

We are now leaning into incubation, backing AI-native service startups before operations begin, but only when the founding teams are stellar operators with a track record in roll-ups.

Why?

Because early is where the asymmetry lies. The next generation of services platforms will be built in the next 12 to 24 months. And because we can help with go-to-market, operations, M&A, and AI strategy, we become part of the founding team’s edge.

With small initial cheques, fast feedback loops, and limited downside, incubation is not just vision. It is a repeatable strategy.

If you’re building

To founders building in this space: you are not alone.

There is a growing cohort of operators rethinking traditional service models through AI. If you are taking on a boring workflow in a big market with a full-stack mindset, we want to hear from you.

Let us build the next generation of AI-native services together.